The Impacts of US Tax Reform on Canada’s Economy

Executive Summary

Our mandate

PricewaterhouseCoopers, LLP (“PwC”, “we” or “us”) was engaged by the Business Council of Canada to estimate the impact of the United States Tax Cuts and Jobs Act (“US tax reform” or the “Act”) on the Canadian economy. The Act was passed in December 2017 with the intention of stimulating greater investment in the US and incentivizing US multinationals to repatriate income held abroad.

In this context, there is potential for the US tax reform to cause a shift in business investment from Canada to the US, resulting in a loss of economic activity in Canada. To assess the extent and likelihood of such consequences, we have taken the following three major steps:

- Identified sectors in the Canadian economy that may be at risk of losing future investment as a result of the US tax reform (“Affected Sectors”).

- Assessed the drivers of investment in these identified sectors and in that context the relative importance of taxes.

- Concluded on the likely impact of the US tax reform on the long-term economic viability of each of the identified sectors.

In addition, we have assessed the impact of changes to personal income tax rates in the US on Canada’s ability to attract and retain high-skilled talent relative to the US, and examined the impact of the US tax reform on the

attractiveness of conducting research and development (“R&D”) in Canada relative to the US.

We have also been asked to provide a list of policy options for consideration by the Canadian federal government in its quest to avoid negative ramifications of the US tax reform on the Canadian economy.

Our findings

Affected sectors

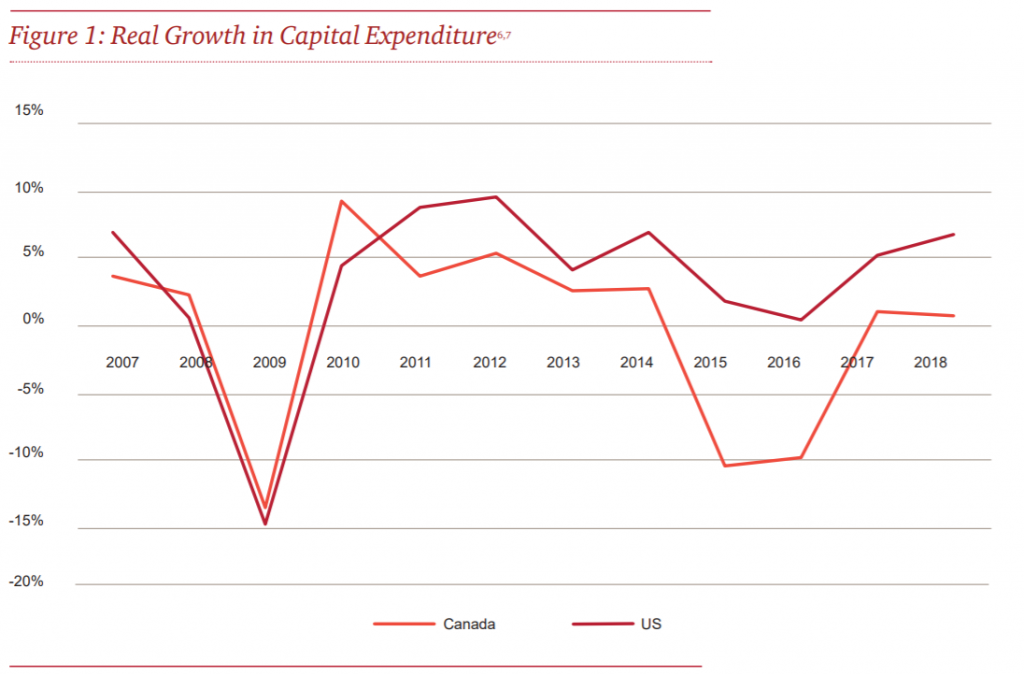

Our analysis suggests that the US tax reform has eliminated one of Canada’s main competitive advantages. We are of the view that this loss will have a significant negative impact on capital-intensive sectors in Canada. All else being equal, these sectors as a whole would likely face a significant shift in investments from Canada to the US over the next 10 years. It is important to understand that the US tax reform comes at the heels of a decade where Canadian capital-intensive sectors were generally lagging their US counterparts in both GDP growth and investment growth. Over the last decade, during which the Canadian corporate tax rate was substantially lower than that in the US, growth in capital expenditures in Canada was significantly slower than in the US. The US tax reform removes a key Canadian advantage, thereby exacerbating the trend of lower investment growth in Canada and threatening the viability of certain parts of Canada’s capital-intensive sectors.

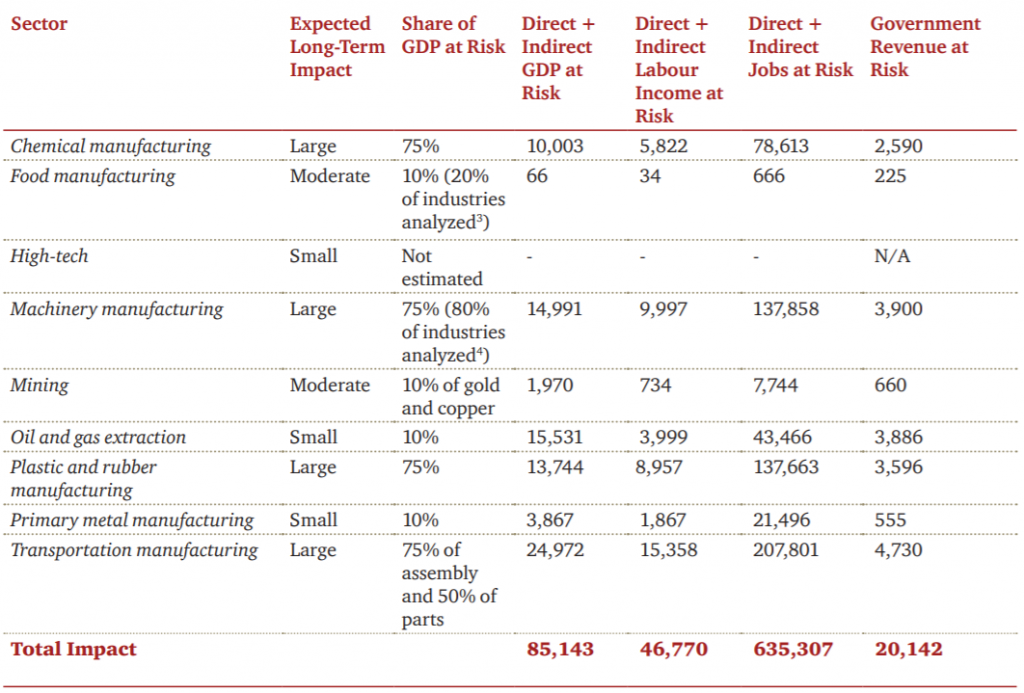

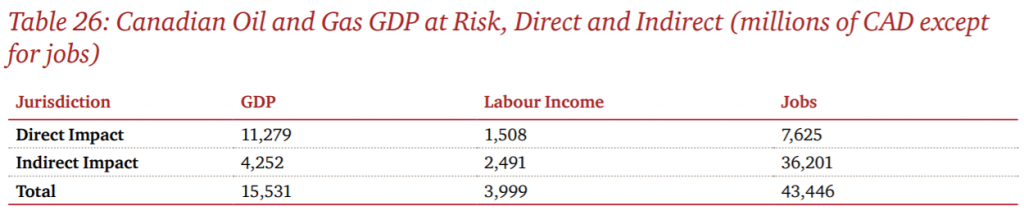

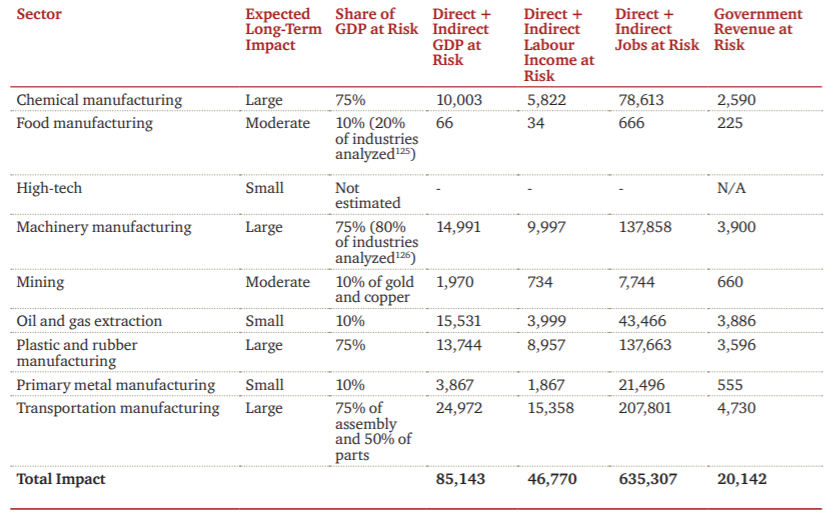

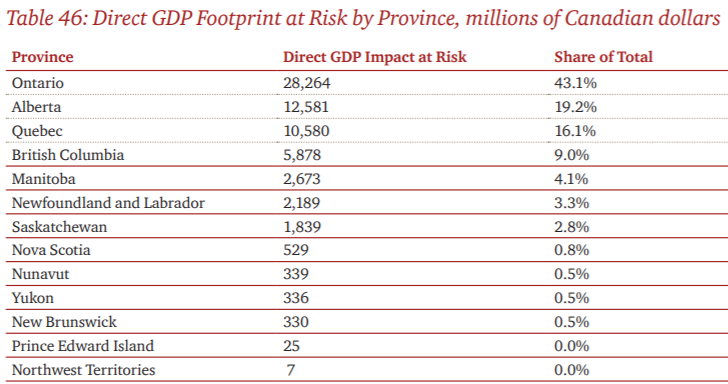

The following table summarizes the existing economic activity that we assess as being at risk of becoming unviable. It includes both the at risk portions of the Affected Sectors (direct impacts) and the activity of Canadian suppliers to those sectors (indirect impacts). In total, we assess that approximately $85 billion CAD in GDP (or 4.9% of Canada’s GDP), 635,000 employees (or 3.4% of Canadian employment), $47 billion CAD in labour income, and $20 billion CAD in government revenue are at risk as a result of the US tax reform. These figures exclude the loss of opportunity to establish new industries or expand existing industries as a result of the digital revolution. Due to data limitations, we have not quantified any loss in the high-tech sector. However, our assessment is that any loss of economic activity in this sector would be relatively minor.

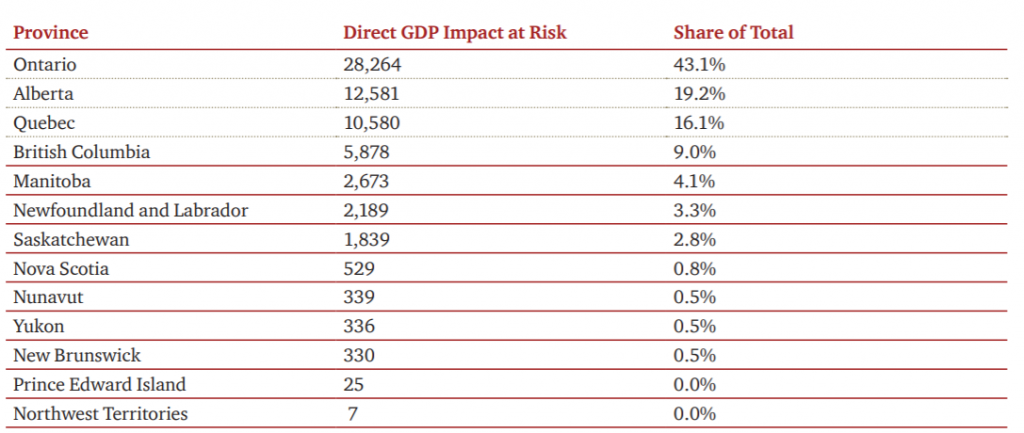

The table below shows the direct GDP impact at risk by province. Ontario, Alberta, and Quebec will experience the largest impacts because of their relatively high concentration of Affected Sectors.

R&D

R&D activity creates high paying jobs and is essential to driving productivity growth. Like most countries, Canada and the US both offer tax credits designed to encourage R&D activity.

Overall, the US tax reform has decreased the net effectiveness of Canada’s SRED (i.e. scientific research and experimental development) credits for US-based companies and increased the net effectiveness of US R&D credits. This is likely to lead to a reduction in R&D activity by US-based companies in Canada, including the spill over benefits that such activity creates. Currently, R&D conducted by US companies in Canada accounts for at least 11% of total private R&D pending in Canada.

Brain Drain

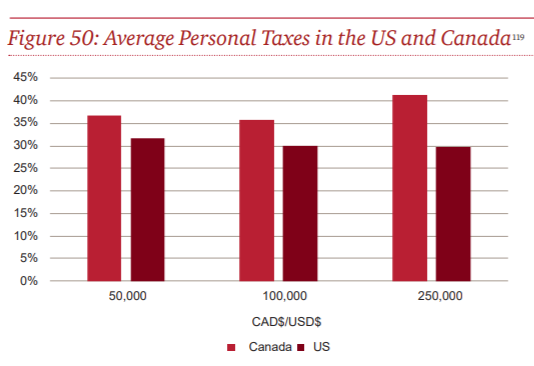

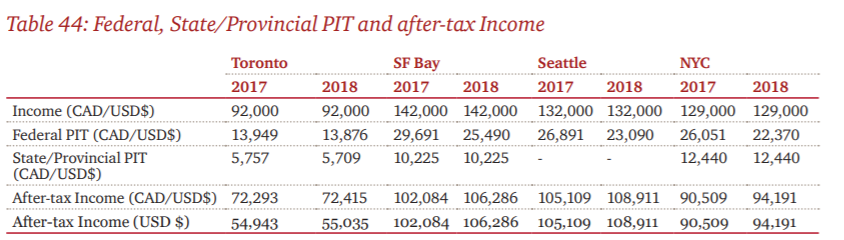

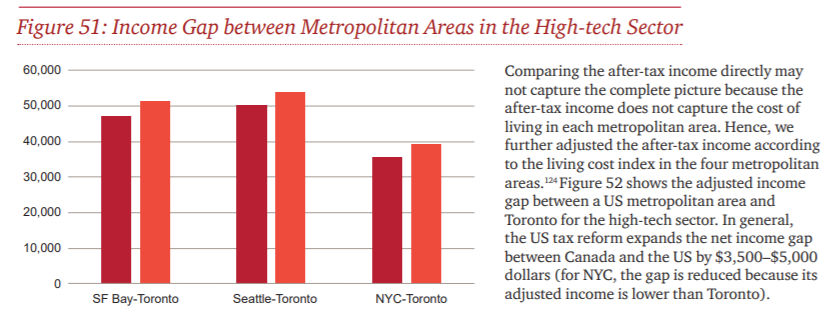

Our analysis suggests that the lower personal income tax rates introduced by the US tax reform will increase the net income gap between the US and Canada, especially in highly skilled occupations. The net income gap is already substantial due to higher wages and lower personal income taxes in the US, which makes the US more attractive to highly skilled workers. The US tax reform therefore marginally increases incentives for highly skilled Canadian workers to relocate to the US and makes it more difficult for Canada to attract highly skilled foreign workers.

The net impact of the US tax reform will likely be limited to an incremental increase in emigration of a few thousand employees per year. However, it will come at a time when Canada needs to reverse the existing brain drain phenomenon in order to ensure that it will emerge a “winner” from the digital revolution that it will likely face over the next 5 to 10 years.

Policy Options

We developed several policy options for consideration of the federal and provincial governments that we believe can act to counteract the negative impacts of the US tax reform. The following is a list of those options:

Tax options

- General corporate income tax measures

- The federal and provincial governments gradually reduce the combined statutory rate to 20% by 1% per year.

- Canada introduces a 100% bonus depreciation for seven years on equipment, structures and acquired intangibles.

- Canada introduces a longer loss carry-back period. A longer loss carry-back period would support resource companies whose earnings are cyclical and can be volatile.

- Brain drain counter measures – personal income tax measures

- Canada increases the personal income tax brackets to closer resemble the US personal income tax brackets.

- The federal and provincial governments reduce the combined top marginal statutory rate to 49%.

- Innovation measures

- Canada reviews its SRED program both from an effectiveness and an administration perspective. The objective is to create a behaviour driving, best-in-class R&D program that, among others, will avoid the negative impact of the US tax reform on the current Canadian SRED program.

- Canada introduces an intellectual property (“IP”) regime (also referred to as a “patent box”).

Funding options

- Tax base expansion measures

- Canada continues to expand its corporate income tax base.

- The federal and provincial governments further increase the personal income tax base.

- Consumption tax measures

- The federal government gradually increases the GST rate.

- The federal and provincial governments agree to introduce one unified carbon tax and use the revenue to reduce

corporate and personal income taxes.

Other policy options

- Administration of income taxes

- Canada (i.e. the Canada Revenue Agency) significantly improves the efficiency and effectiveness of the

administration of Canada’s corporate and personal income taxes.

- Canada (i.e. the Canada Revenue Agency) significantly improves the efficiency and effectiveness of the

- Regulatory approvals

- Canada’s federal, provincial and territorial governments significantly simplify and shorten approval processes for

large-scale projects and reduce the uncertainty of the outcome of these processes.

- Canada’s federal, provincial and territorial governments significantly simplify and shorten approval processes for

Introduction

PricewaterhouseCoopers, LLP (“PwC,” “we” or “us”) was engaged by the Business Council of Canada to estimate the impact of the United States Tax Cuts and Jobs Act (“US tax reform” or the “Act”) on the Canadian economy. The Act was passed in December 2017 with the intention of stimulating greater investment in the US and incentivizing US multinationals to repatriate income held abroad.

In this context, there is potential for the US tax reform to cause a shift in business investment from Canada to the US, resulting in a loss of economic activity in Canada. To assess the extent and likelihood of such consequences, we have taken the following three major steps:

- Identified sectors in the Canadian economy that may be at risk of losing future investment as a result of the US tax reform (“Affected Sectors”).

- Assessed the drivers of investment in these identified sectors and in that context the relative importance of taxes.

- Concluded on the likely impact of the US tax reform on the long-term economic viability of each of the identified sectors.

In addition, we have assessed the impact of changes to personal income tax rates in the US on Canada’s ability to attract and retain high-skills talent relative to the US, and examined the impact of the US tax reform on the attractiveness of conducting research and development (“R&D”) in Canada relative to the US.

In conducting our analysis, we have focused on the impacts of the changes to the US tax code that are most likely to affect investment in Canada, as follows:

- The lowering of the statutory corporate income tax rate.

- The introduction of immediate capital expensing.

- The deduction related to export earnings.

Other changes to the US tax code were assessed on a high level as to their general directional impact.

We have also been asked to provide a list of policy options for consideration by the Canadian federal government in its quest to avoid negative ramifications of the US tax reform on the Canadian economy.

All dollar figures are in 2017 US dollars unless otherwise specified. Conversions have been made at the purchasing power parity (“PPP”) rate, which equalizes prices between two countries, thereby holding purchasing power constant. The 2017 Canadian exchange rate we have used is $1.25. Any “pre-reform” US tax rates in this report refer to 2017 US tax rates.

The key authors of this study are:

- Michael Dobner, National Leader, Economics Practice, PwC Canada

- Peter van Dijk, National Leader, Tax Policy, PwC Canada

- Gemma Stanton-Hagan, Senior Economist, PwC Canada

- Manpreet Kaur Juneja, Economist, PwC Canada

- Angelo Bertolas, Senior Tax Advisor, PwC Canada

Scope of review

To prepare this assessment, we have reviewed and, where appropriate, relied upon various documents and sources of information. By general classification, these sources include the following:

- IBIS

- Statistics Canada

- Bureau of Economic Analysis

- US Census Bureau

- US Energy Information Administration (“EIA”)

- Organization for Economic Cooperation and Development (“OECD”)

- World Bank

- Interviews with industry participants

- Academic research articles

- News articles

A full list of sources and articles used for the purpose of this assessment is available in Appendix A: References.

U.S. Tax Reform

In December 2017, the Tax Cuts and Jobs Act was signed into law in the United States (“US”). Its purpose was to stimulate investment in the US and incentivize US multinationals to repatriate income held abroad. In industries where Canada and the US compete for capital, the changes introduced by this reform may have an impact on the relative attractiveness of Canada and the US as alternative destinations for investment.

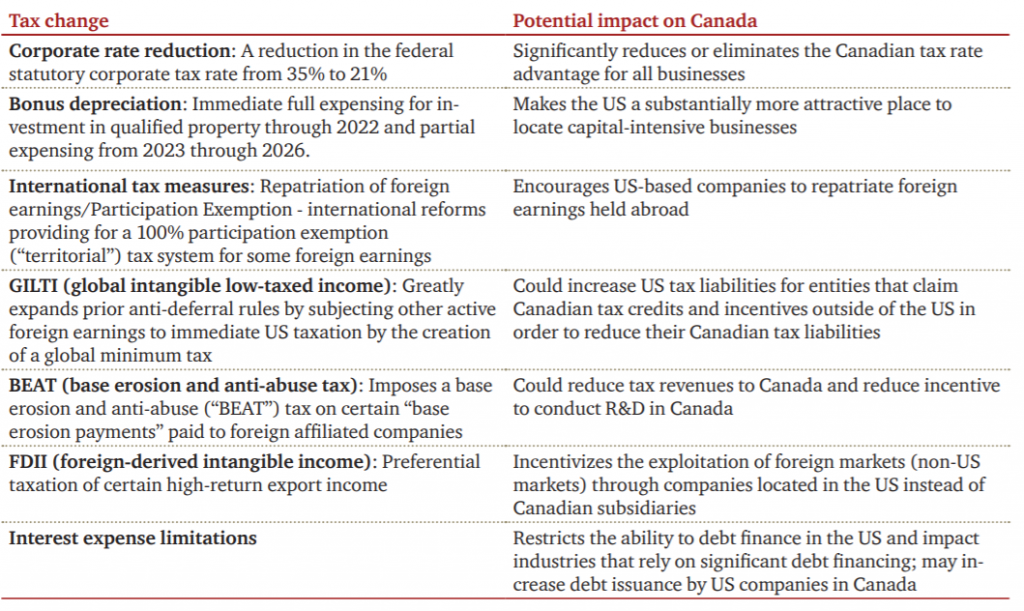

Prior to US tax reform, Canada’s statutory corporate tax rates were substantially lower than in the US, increasing Canada’s attractiveness to new investment. Due to the US tax reform, Canada’s tax advantage has been eliminated. Below we list the components of the US tax reform that are most likely to influence Canada’s competitiveness in attracting investment. A more detailed description is provided in Appendix C: US tax reform measures.

Other measures introduced through the US tax reform are likely to have a minor impact, if any, on Canada’s economy.

The State of Canadian Competitiveness

The following section reviews the state of Canada’s overall competitiveness in relation to the US. We first review overall rankings of national competitiveness and the reasons for Canada’s place in them. We then assess the factors contributing to individual companies’ investment decisions.

This report focuses on Canada’s investment competitiveness because Canada needs to compete with other countries for the capital investment necessary to create economic growth and jobs. It is important to note that prior to US tax reform, Canada had been lagging behind the US in terms of both business investment and economic growth for several years, as shown in Figure 1 and Figure 2.

Canada’s competitiveness in this report refers to its ability to attract new investment. In today’s global economy, Canada competes with the US and other jurisdictions for potential new investment in many industries.

The Global Competitiveness Index published by the World Economic Forum ranks economies based on national competitiveness. In 2017—18, out of 137 economies, it ranked the US as the second most competitive nation while Canada was ranked 14th. The US’s ranking has improved from 7th in 2012 – 13 while Canada has remained stagnant at 14th.

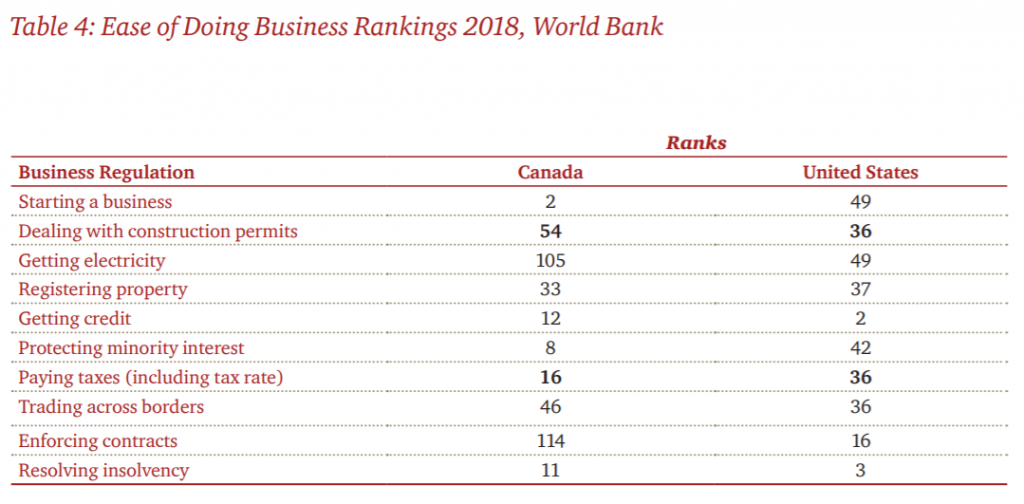

At a disaggregated level, this disparity in ranking reflects productivity differences in various factors summarized in Table 3. While Canada has higher competitiveness than the US for basic requirements, it lags behind on efficiency enhancing factors and innovation and sophistication. For total tax rate, a goods market efficiency enhancing factor, the US was ranked 95th in 2017 while Canada was 15th. The Executive Opinion Survey 2017 reported tax rates and tax regulations as the two most problematic factors for doing business in the US.

The International Tax Competitiveness Index (“ITCI”) measures two important aspects of a country’s tax system: competitiveness and neutrality. In 2017, out of 35 OECD countries, Canada was ranked 17th and the US 30th for international tax competitiveness.

As shown in the above tables, Canada’s corporate tax advantage relative to the US was a key factor in reducing the gap in competitiveness between the US and Canada. The US tax reform has eliminated this one important Canadian advantage.

The United Nations Conference on Trade and Development World Investment Report 2018 points out that about half of global foreign direct investment (“FDI”) stocks are either located in the US or owned by US multinational corporations (“MNCs”). The conference expects the US tax reform to significantly impact investment in the rest of the world. The US tax reform will increase post-tax return in the US relative to other countries, thereby making them less attractive to investment relative to the US. In particular, the tax exemption on repatriation could encourage US MNCs to repatriate more than $3.2 trillion of accumulated overseas retained-earnings to the US.

Investment decisions

In industries where Canada competes with the US for new investment, businesses carefully weigh the expected return on investment before deciding where to locate a new facility or expansion. Typically, this is done using a cash flow model. In most cases, the following considerations are important in these decisions:

- Market size and accessibility to customers. Large corporations are generally more productive than small and medium-sized businesses. Due to the larger size of the US market, the average size of firms in the US is larger compared to Canada. This factor is estimated to account for about 50% of the corresponding manufacturing productivity gap and 20% of the gap in sales per employee.

- Non-location sensitive costs. Some operating costs, such as raw materials, parts, sub-components, major plant and equipment, do not vary significantly by location. These tend to be governed by world market prices or are fixed at other levels of the supply chain.

- Location-sensitive costs:

- Labour costs, including salaries, employee benefits and statutory plans

- Facility costs, including land, construction, lease, rental costs

- Transportation costs

- Utility costs

- Cost of capital, including financing cost, depreciation charges

- Tax rates

- Incentives

- Regulatory costs

- Availability of key resources:

- Land

- Skilled labour

- Suppliers

Based on interviews with company executives, Canada’s relatively low corporate tax rate was an important element of Canada’s attractiveness for investment prior to the US tax reform. Therefore, considering the geographical proximity and overall competitiveness of the US economy, the US tax reform that eliminates a major advantage for Canadian businesses relative to US businesses may pose a significant risk for the Canadian economy.

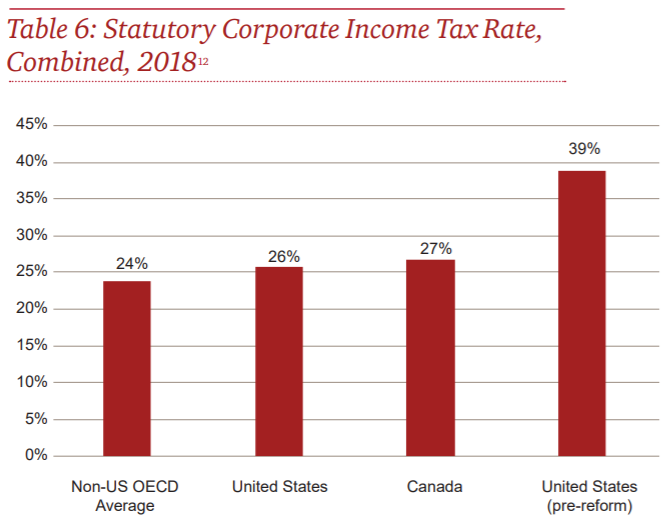

The chart below illustrates the combined national and sub-national statutory corporate income tax rate in Canada, the US (both pre- and post-tax reform) and the non-US OECD average. Canada’s rate is now above both the OECD average and the US rate, whereas previously the US rate was substantially higher.

NAFTA renegotiations and tariffs

As noted above, access to market is a key component of investment decisions, particularly in an increasingly globalized market. Currently, there are a number of potential changes to the North American trading environment. NAFTA renegotiations are ongoing, and the US has introduced tariffs of 25% and 10% on steel and aluminium, respectively. There is an ongoing section 232 investigation that could result in tariffs of up to 25% on Canadian auto and auto parts exports to the US. Above all, the uncertainty created by this kind of environment is detrimental to investment in Canada and is among the top concerns of companies we interviewed for this study. If these issues are not resolved favourably for Canada, they will act as another obstacle to the Canadian economy over and above the US tax reform. However, for the purposes of this study, we have assumed that all trade disputes between Canada and the US will be resolved with no significant negative impact to Canada.

Technology and new investment

The term “Industry 4.0” refers to the increasing digitization and automation in industrial production, and encompasses a wide range of changes to technology and process. Innovation and advances in technology will shape the economy of the future, while companies that fail to embrace these changes will fall behind.13 Therefore, these trends increase the importance of attracting new investment in the coming years. The impact will be especially large in manufacturing industries, which have the highest potential for digital transformation. This is expected to lead to a return of significant portion of production that was lost to developing countries in previous decades back to North America.

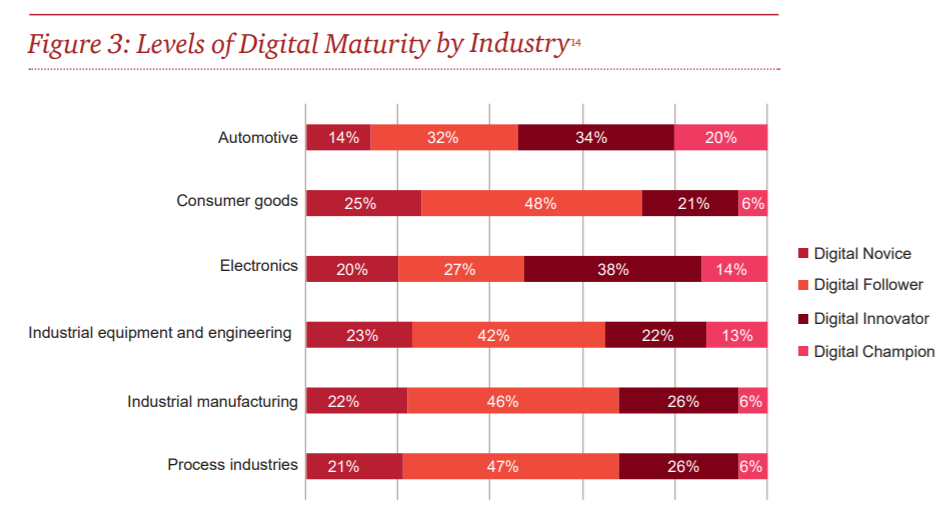

Figure 3 shows the level of digital maturity by industry. Automotive, electronics and industrial equipment are among the most digitally advanced industries globally.

Industry 4.0 affects new investment in the following ways:

- Creates a need for substantial new investment, even in mature industries where technology is employed to lower costs.

- Increases the capital intensity of new investment.

- Increases the importance of high-skilled labour.

As this report shows, US tax reform is expected to have a particularly large impact on capital-intensive industries, and may increase the “brain drain” of highly skilled workers from Canada to the US. Therefore, greater digitization exacerbates the threat to Canada posed by US tax reform not only in losing portions of its existing industries but also in foregoing the opportunity to “onshore” activity that has been outsourced to developing countries.

Impact of US tax reform on investment

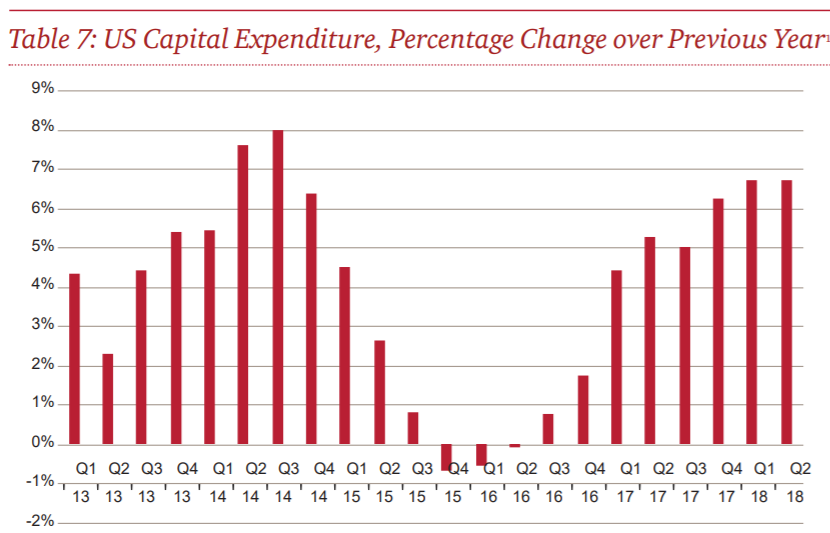

The following section reviews the literature on the impact of corporate income tax cuts on investment. Economists generally agree that a decrease in the effective corporate income tax rate will lead to an increase in investment, but not necessarily on the magnitude of the impact. Changes in the corporate tax rate influence investment through two channels. First, they increase the expected after-tax return on any future investment. This is the focus of the analysis in this report. Second, tax cuts increase companies’ cash flows by decreasing taxes on investments that they have already made.15 Recent data supports the idea that the tax cuts will encourage investment: a PwC survey of 20 US large-cap companies showed that 45% plan to increase investment, while another 45% plan to return money to shareholders and 10% plan more acquisitions. Capital expenditure of S&P 500 companies in the first quarter of 2018 was up 21% year-over-year, and represents the largest one-quarter increase in seven years. The table below shows the change in capital expenditure over the previous year by quarter. The first two quarters of 2018 following the US tax reform show strong growth compared to the previous three years.

A report by Bloomberg applied estimates from literature to the current US tax reforms and predicts an increase in investment of 6% for US corporations and 32% for US multinationals, based on temporary bonus depreciation and not including the macroeconomic impacts of deficit spending.

Cummins, Hassett and Hubbard looked at the impact of corporate tax cuts in the US in 1961, 1971, 1981 and 1986. They found that on average, all else being equal, a one percentage point decrease in the corporate tax rate increased capital investment by between 0.5% and 0.8%percentage points, and that the impacts were significantly larger for firms with no tax loss carry forwards. More recently, Lewellen and Lewellen used US data from 1971 to 2009, using lagged returns and lagged cash flow as instrumental variables to correct for bias in the data. They found that one dollar of current and prior year cash flow is associated with between $0.32 and $0.63 of investment for firms that were less borrowing constrained and more borrowing constrained, respectively. Djankov et al. looked at corporate tax rates across many countries and found that a 10 percentage point increase in corporate taxes was associated with aggregate investment that was two percentage points lower. Higher corporate tax rates were also associated with lower levels of FDI and entrepreneurship, and were found to impact manufacturing, but not services.

Ljunqvist and Smolyansky use a novel approach that takes advantage of spatial discontinuity in the tax rate between adjacent US counties using data from 1970 to 2010. They found that corporate tax cuts have no impact on economic activity unless they are implemented during a recession, in which case they significantly increase employment, and income.

Given the high level of globalization in the US, FDI is also important. Razin, Sadka, Desai and Swenson found that an increase in the corporate tax rate in the host country had a significant negative impact on FDI. An increase in the corporate tax rate in the source country had a positive effect, as we would expect to see when countries compete for capital investment.

Overall, the literature supports the idea that a decrease in corporate tax rates should increase investment, including FDI. However, the precise magnitude is not clear, and a number of factors such as loss carry-forwards at a given company, a lack of borrowing constraints, and an economic expansion could dampen the effects. Given Canada’s proximity to the US and high level of integration with the US economy, it is likely that an increase in investment in the US would likely come mainly at the expense of Canada.

Impacts of Deregulation

Along with tax reform, the current US administration has prioritized widespread deregulation. At the same time, the current Canadian government has introduced new regulations that will negatively affect energy consuming industries and resource extraction industries. While trends in regulation in both countries will likely impact investment decisions, detailed analysis of regulatory cost is outside of the scope of this report. Instead, regulatory issues that are likely to affect cost competitiveness are discussed on a case-by-case basis for each industry. The section below summarizes some key regulatory changes recently made in the US and Canada. We note that there may be negative long-term consequences of some deregulation that outweigh short-term cost savings. It is not our view that Canada should pursue a similar program of deregulation. However, regulation is an important component of attractiveness to investment, and recent changes are likely to have an impact.

In 2017, the US government issued 67 deregulatory actions, which the Office of Information and Regulatory Affairs estimates will save government agencies $570 million per year.25 Those most relevant to the industries studied in this report are regulations governing the environment and labour. On the environmental side, the Trump administration continues to work to repeal the Clean Power Plan, an Obama-era rule requiring coal-burning power plants to decrease carbon emissions. The US government is also revising the Obama-era expansion of the definition of “navigable waters” under the Clean Water Act, with the aim of decreasing protected waters. In the oil and gas industry, the government has proposed a revision to the Methane Rule, which regulates the waste of natural gas from venting, flaring, leaks, and emissions during oil and gas production. Additionally, there is a proposal to expand oil and gas drilling in the Outer Continental Shelf, which would allow drilling in more than 1 billion acres that were previously off-limits. On the labour side, the Trump administration has nullified a rule designed to improve federal contractor compliance with labour laws, and modified a rule requiring safety and health examinations of mines to be conducted before miners begin work. Anecdotally, we understand that these changes have encouraged investment in the US metals industry, but it will take many years to understand the full extent of their impact.

There have not been as many changes on the Canadian side. However, certain recent changes are likely to affect investment. The Canadian government recently introduced Bill C-69, which would change the approval process for mining and oil and gas projects. Once the bill is enacted in 2019, a government agency will review proposed projects’ environmental, health, social, and economic impacts over the long term. Critics say this will increase costs and uncertainty for resource companies. The Canadian government has also mandated that each province legislate either a carbon tax or cap-and-trade scheme in order to reduce carbon emissions. In addition to creating costs for companies, this policy has created uncertainty because some provinces are considering legal action to opt out of the program. Additionally, Ontario recently enacted major labour market reforms including raising the minimum wage, requiring that full-time and part-time workers be paid the same hourly wage, and increasing paid time off.

Approach and Methodology

The principal question that this report aims to answer is the potential impact of US tax reform on the Canadian economy. This study assesses three main impact channels:

- The direct impact of US tax reform on investments in Canada given the increase in US after-tax returns.

- The impact of US tax reform on the effectiveness of R&D incentives in Canada and its impact on R&D activity taking place in Canada.

- The impact of changes to personal income tax rates on Canada’s ability to attract and retain high-skills labour.

1. Direct impact on investment

A decrease in the corporate tax rate in the US, as well as other changes brought in by the Act, significantly increases the after-tax return on investment in the US relative to Canada. This is the main channel that our study investigates. Our approach to estimating this impact is on a sector-by-sector basis, and we used the following steps:

- Identified the Canadian sectors where investment is most likely to be directly affected by the US tax reform. Our approach to this step is described in the section on Affected Sectors.

- Assessed the trends in the Affected Sectors prior to the US tax reform and identified the key factors companies consider when deciding where to locate investment.

- Interviewed executives of key companies in each sector about their considerations when making investments.

- Gathered anecdotal information on shifts in investment that appear to be related to the US tax reform.

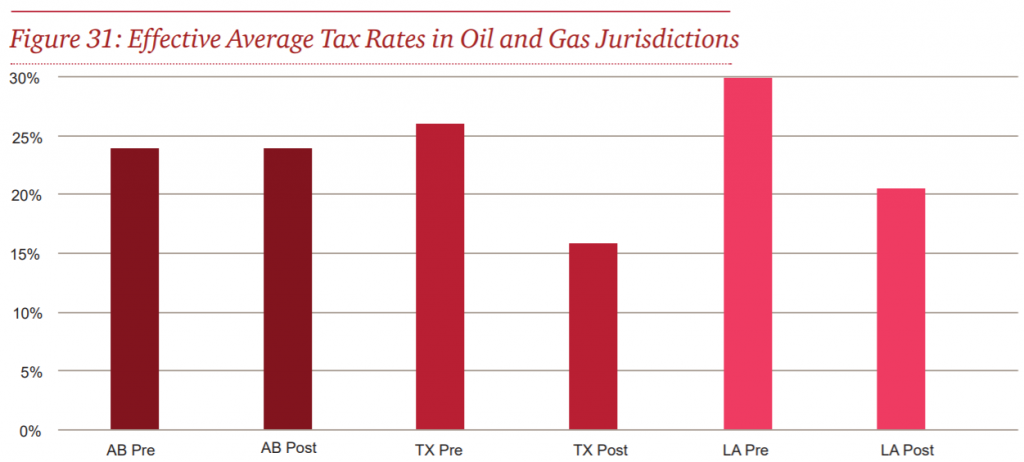

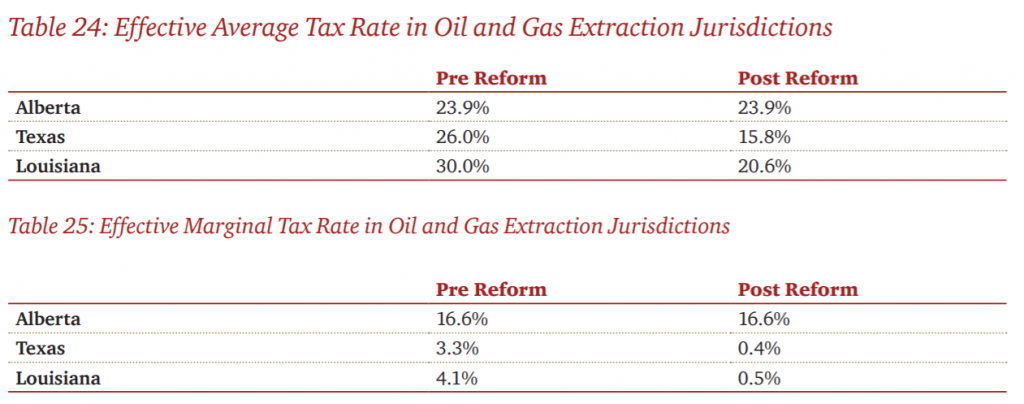

- Compared the effective average tax rates and effective marginal tax rates in relevant jurisdictions in Canada, and in the US pre-US tax reform, and post-US tax reform.

- Compared pre-tax profitability in relevant jurisdictions.

- Based on the above, concluded on the magnitude of likely direct impact on each sector.

- Based on the estimated impact, assigned an approximate share of the sector’s economic footprint that we predict will be at risk.

2. Impact on R&D incentives

Although the US tax reform has not immediately changed direct R&D incentives, the lowering of the corporate tax rate increases the effectiveness of existing US R&D credits. The Act also changes the way that foreign income of US companies is taxed through FDII and GILTI provisions, thereby changing the effectiveness of Canadian R&D credits for US-based companies. We assessed the impact of these changes through quantitative modelling of the R&D credits available on a certain investment in Canada and the US, both before and after US tax reform.

3. Personal income tax and the brain drain

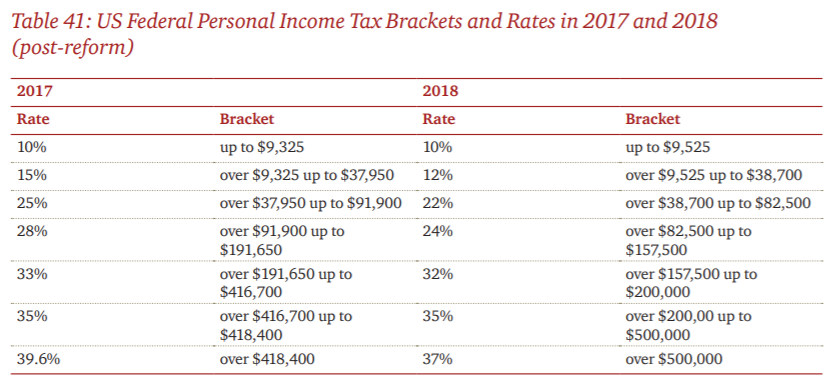

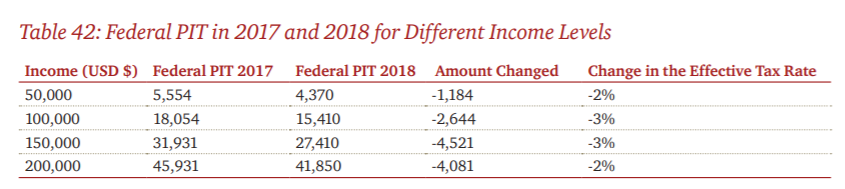

In addition to changes to corporate income taxes, the US tax reform also lowers personal income tax rates and raised some bracket thresholds. This could have impacts on Canada’s ability to attract and retain high-skills labour, given the already large gap in after-tax income between Canada and the US in high-skilled occupations. We assess existing trends in competition for high-skilled labour and the relative attractiveness of Canada and the US. We then quantify the existing gap in after-tax income between the US and Canada and the increase in this gap caused by US tax reform, and conclude on the potential economic impacts.

Limitations

The following factors are out of the scope of this study:

- Changes to NAFTA and tariffs: We have assumed that all trade disputes between Canada and the US will be resolved with no significant incremental negative impact to Canada.

- Costing of regulations: We have not quantified the impact of recent and anticipated changes to regulation in the US and Canada, although we considered them qualitatively in our analysis.

- All measures included in the US tax reform including temporary measures such as bonus depreciation will remain in place for the foreseeable future.

- We have not taken into account any potential policy changes made by governments in Canada in response to the US tax reform.

- We have not considered the opportunity cost resulting from the potential for repatriation of sectors that do not currently have a substantial footprint in North America, because of technological advancements such as machine learning and artificial intelligence.

- The Canadian dollar will trade at its “fair economic value” as measured by the PPP rate.

Affected Sectors

This section describes our approach to identifying which sectors are likely to be most directly impacted by the US tax reform. The industries that we identified as likely to be directly impacted are assessed in the section on Impact of US tax reform on the competitiveness of Affected Sectors. We note that other sectors will be affected indirectly by a change in demand from directly affected sectors through the supply chain.

Our first step in identifying the Affected Sectors was to eliminate sectors that are local in nature and must serve their customers in the area of residence. In sectors where that is the case, Canada does not compete with the US for investment. We note that to the extent that these services are being outsourced, they are likely to be provided from a country with substantially lower-cost labour rather than the US. This criterion eliminated the following two-digit North American Industry Classification System (“NAICS”) categories:

- Utilities

- Construction

- Wholesale trade

- Retail trade (not including online retail trade)

- Transportation and warehousing

- Real estate, rental and leasing

- Management of companies and enterprises

- Administrative support, waste management and remediation services

- Educational services

- Health care and social assistance

- Arts, entertainment and recreation

- Accommodation and food services

- Other services (except public administration) that includes repair and maintenance, personal and laundry services, religious, grant-making, civic, professional and similar organizations, private households

- Public administration

- Professional, scientific and technical services that includes legal, accounting, tax, architectural, engineering, design, consulting, R&D, advertising, public relations and others, are local services mostly provided in the territory of demand.

In addition, we have excluded the financial and insurance industries because of regulatory barriers between the US and Canada and relatively low growth caused by saturation in the Canadian market.

After these eliminations, four two-digit NAICS categories remained:

- Agriculture, forestry, fishing and hunting (no industry included after further analysis explained below)

- Mining, quarrying, oil and gas extraction

- Manufacturing

- Information and cultural industries (included because of the high-tech industry)

In order to assess these industries, we analyzed the sub-sectors (three-digit NAICS) that comprise them using the following criteria:

- Canadian GDP greater than $10 billion CAD.

- Whether Canadian and US products are competing on North American or export markets.

- Profit margins: similar margins in Canada and the US suggest competitiveness.

- Presence of multinational companies: Their presence suggests that major players allocate investment internationally.

- Structural trends: We aimed to exclude industries that are not attracting new investment into Canada. Regardless of the US tax reform (e.g., coal mining), and those where there are regulatory or policy barriers to capital mobility (e.g., shipbuilding).

- Capital intensity: Those with high capital intensity are more likely to be impacted because of bonus depreciation.

The following sectors have a large footprint in trade and GDP, but were excluded because of secular trends that limit the potential impact of US tax reform:

- Petroleum and coal product manufacturing. By far the largest component of this industry is petroleum refineries, which are among the top exporters of Canada. However, only one new petroleum refinery has been built in the last 30 years, and some analysis suggests there is already overcapacity. It appears that US refineries are already more cost-effective even before the tax reforms. We note that if oil and gas production is negatively impacted, petroleum refining would also decrease.

- Crop production. This market is relatively less trade-reliant, as major companies in Canada have no presence in the US and imports are low.

- Wood product manufacturing. Estimates suggest that production capacity in British Columbia will be decreasing between now and 2020 because of limitations on wood supply. Recently there has been more investment in the US south because of greater wood supply, although Canada is still cost-competitive.

Based on the above criteria, we have defined the following sectors as likely to be directly affected by US tax reform (i.e. the Affected Sectors), in alphabetical order:

- Chemical manufacturing

- Food manufacturing

- High-tech

- Machinery manufacturing

- Mining

- Oil and gas extraction

- Plastic and rubber manufacturing

- Primary metal manufacturing

- Transportation equipment manufacturing

Some industries within these sectors are excluded, as described in the following sections.

Impact of US tax reform on the competitiveness of Affected Sectors

In this section, we present our findings regarding each of the Affected Sectors and the key industries within each.

The description of each sector is organized as follows:

- The sector in Canada: describes the activity in Canada and identifies key jurisdictions.

- The sector in the US: describes the activity in the US and identifies key jurisdictions.

- Investment trends: reviews recent trends in capital expenditure in Canada and the US.

- Key sector trends: identifies important drivers of activity and investment in the sector.

- Investment decisions: assesses which factors are important when deciding where to locate new investment.

- Rate of return: compares key jurisdictions in terms of pre-tax rate of return in order to assess the likely impact of tax changes.

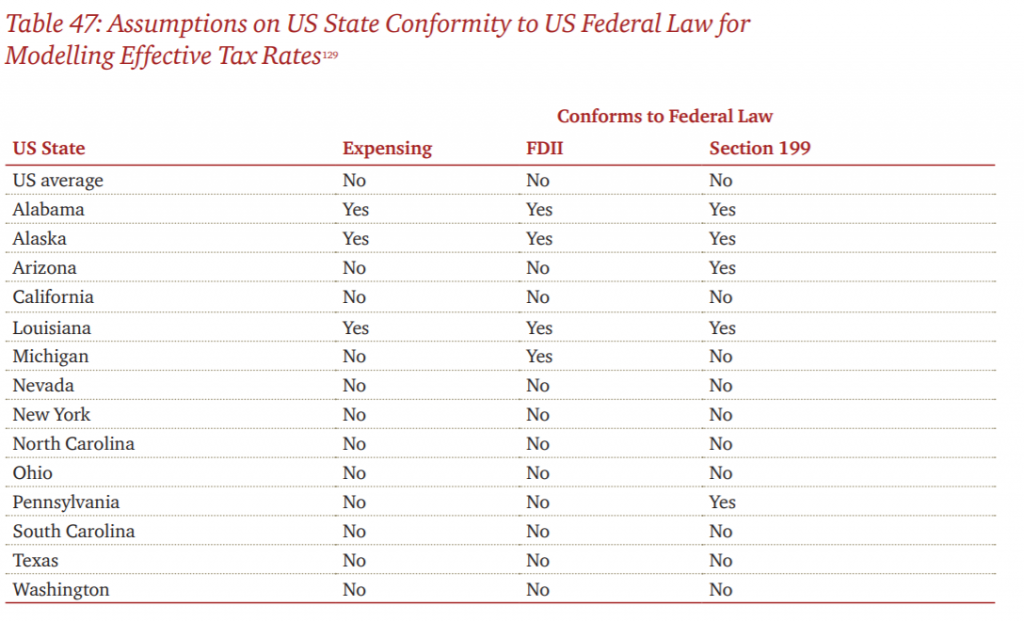

- Tax impact and likely expectations: assesses the impact of tax reform on tax rates in the sector and concludes on the likely impact of tax reform. In that regard, we present the effective average tax rates and effective marginal tax rates in each sector. We note that the effective average tax rate shows the overall average rate a company would pay, and is most relevant for highly profitable companies when they are deciding where to locate a new investment. The marginal tax rate represents the tax paid on an additional dollar of profit, and is more relevant when deciding how large a given investment will be, or whether to expand on an existing site. We also present the effect on US tax rates under the assumption that marginal revenues are being generated through exports. In this regard, we take into account the FDII export-based credit. This analysis is relevant where a possible shift of revenues currently generated in Canada from domestic sources is shifted to the US and exported back into Canada.

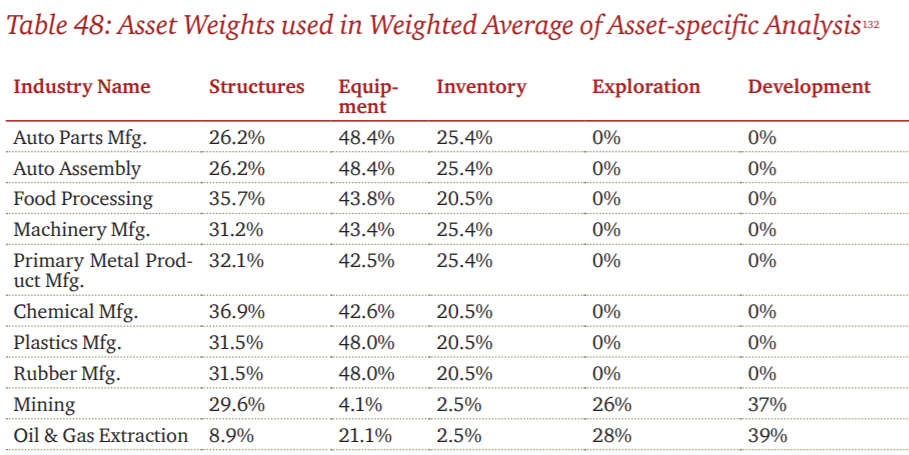

- Conclusions and GDP impact: states our view of the likely impact of tax reform on the sector and identifies the share of the sector’s GDP, employment, and labour income footprint that we view as being at risk. Our methodology for assessing this impact is described in Appendix D: Input output methodology

Chemical manufacturing

Chemical manufacturers transform raw materials into consumer chemical products. The following are the three main activities within chemical manufacturing:

- Petrochemicals

- Pharmaceutical manufacturing

- Other chemical manufacturing including cosmetics, soap, adhesives, paint, fertilizer, synthetic fibres, and other chemicals

Our analysis focuses on petrochemicals and other chemicals. Pharmaceutical manufacturing has been excluded because new manufacturing capacity is not being added in Canada or the US, and this trend has not been affected by the US tax reform. However, new investments are being made in both petrochemicals and other chemicals, and the US and Canada are in competition for new capital investments. These two sub-sectors are discussed separately because different factors affect their competitiveness.

Chemical manufacturing in Canada

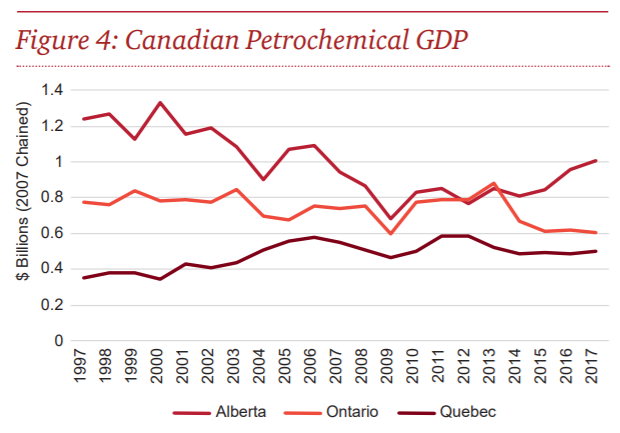

Petrochemical manufacturing transforms crude oil and natural gas into chemical products, which are then used to manufacture industrial and consumer goods. Ethylene and propylene account for 59% and 20% of Canadian petrochemical production respectively.

Petrochemical manufacturing occurs mainly in Alberta and Ontario with some activity in Quebec. In the past five years, GDP in Alberta has been on an upward trend, while in Ontario and Quebec it has remained approximately flat.

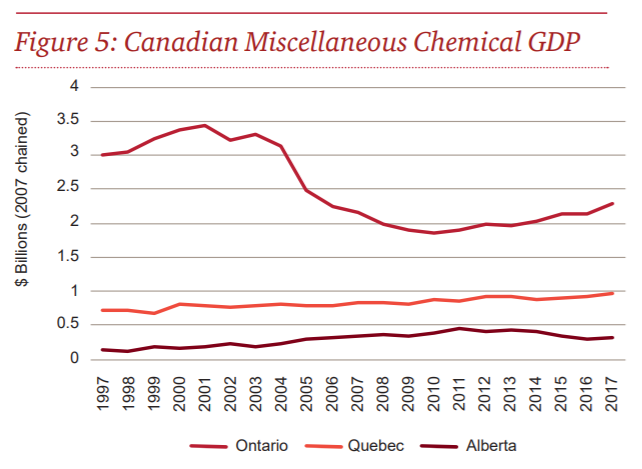

Although locations vary depending on the industry, most other chemical manufacturing is located in Ontario and Quebec. Unlike petrochemical manufacturing, these industries do not rely heavily on access to raw materials.

Chemical manufacturing in the U.S.

In the US, new investment in petrochemical manufacturing is occurring mainly in Texas and Louisiana. As in Canada, close proximity to raw materials (feedstock) is an important factor for competitiveness.

Other chemical manufacturing varies by industry, but primarily occurs in Texas, New York, California, and New Jersey.

Investment trends

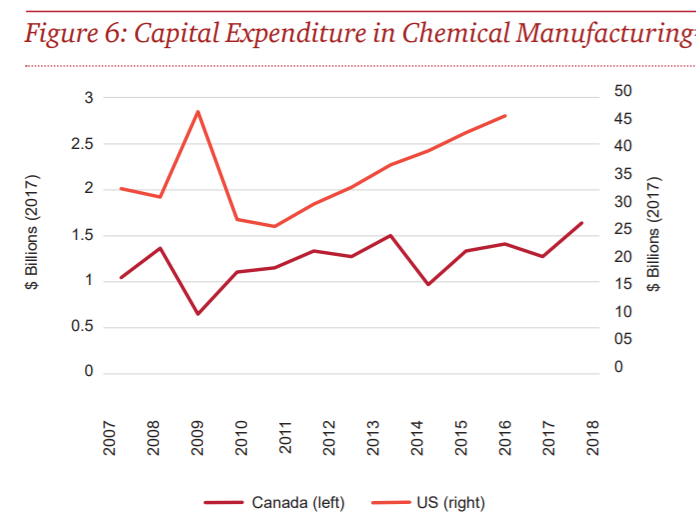

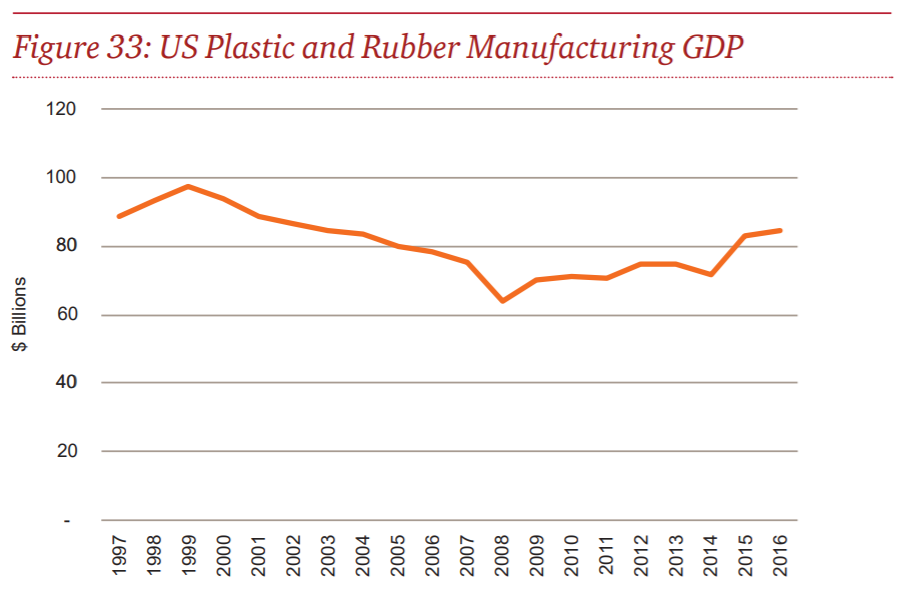

Capital expenditure in chemical manufacturing in Canada has been steady since around 2011, with an uptick in expected 2018 capital expenditure driven by activity in Alberta and Ontario. Capital expenditure in chemical manufacturing in the US has been steadily increasing since 2011, and was over $45 billion USD in 2016. Between 2011 and 2016, investment in the US increased by 51% while investment in Canada increased 6%, suggesting that prior to US tax reform, Canada was already perceived by investors to be less competitive.

Although US data is only available up to 2016, research suggests that US capital expenditure in the petrochemicals industry continued on its trend of strong growth.

Key sector trends

Petrochemical manufacturing

Currently, evidence suggests that prior to tax reform Canada was slightly less attractive than the US as a destination for new petrochemical facilities. Research by the Canadian Energy Research Institute (“CERI”) found that the cost of building a new petrochemical facility in Alberta or Ontario is significantly higher than the US Gulf Coast, taking incentives and rebates into account. A different CERI report looked specifically at methane-based petrochemicals and found that the internal rate of return (“IRR”) was higher in the US Gulf Coast than in Canada, and that tax reform would negatively impact this return across the board.

The relative attractiveness of the US is reflected in the fact that, capital expenditure in chemical manufacturing has decreased by 0.3% in Canada over the past five years, while increasing by 10.0% in the US. Below, we review the industry trends that have contributed to this situation.

Feedback prices

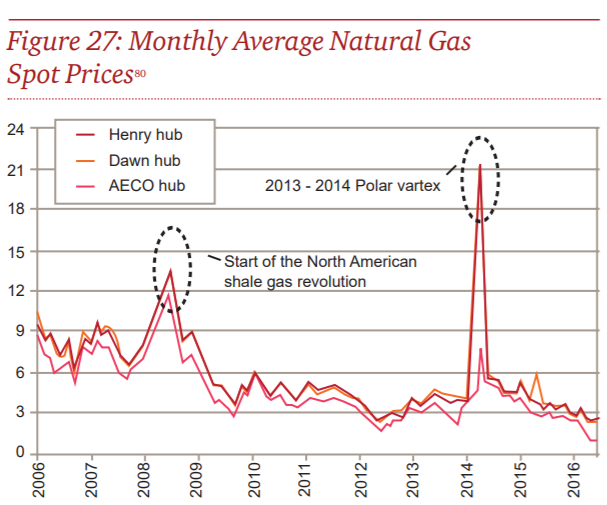

The main input into petrochemical manufacturing is feedstock, which is derived from either natural gas or crude oil. Therefore, the prices of natural gas and crude oil have a major impact on cost competitiveness. The majority of Canadian petrochemical manufacturing uses ethylene as feedstock, which is derived from natural gas liquids that are produced during natural gas processing. In Ontario, 40% of production uses benzene and toluene, which come from petroleum refineries. In contrast to Canada, more US facilities use naphtha as feedstock, which is derived from crude oil, meaning that US costs decrease when crude oil prices decline.

Since the shale revolution in the mid-2000s, natural gas prices in North America have remained below $4/btu (i.e. British thermal unit), compared to over $6/btu prior to 2009. Currently, natural gas prices in Canada are even lower, partially due to difficulty in getting natural gas to market. Canada’s only export market is the US, which also has plentiful low-cost natural gas. This dynamic is expected to change if proposed liquefied natural gas (“LNG”) facilities are built in British Columbia. Such facilities would enable Canadian producers to export to Asia. The proposed capacity for the planned initial facility is 3.23 billion cubic feet per day (“bcfd”), which amounts to 10% of global supply. Although such a facility would benefit natural gas producers, it would also raise the cost of feedstock for petrochemical producers. Several LNG facilities are also planned or under construction in the US, with export capacity expected to rise to 9.4 bfpd (i.e. barrels of fluid per day) by the end of 2019. While this will likely impact natural gas feedstock prices in the US, proposed export capacity as a share of production is significantly higher in Canada, meaning that natural gas prices will increase more for Canadian petrochemical producers compared to their American competitors.

Government support

Governments in both Canada and the US offer incentive programs for investment in petrochemicals. In Alberta, the Petrochemical Diversification Program has offered $500 million to companies opening new petrochemical facilities. Ontario also offers incentive programs to encourage new investment. In recent years, companies have not invested in new petrochemical facilities in Canada without government incentives.

In the US, Texas and Louisiana also offer incentive programs, such as the Texas Enterprise Fund and Chapter 313 of the tax code that offers tax breaks for investment that creates jobs.

Regualtion

Regulatory uncertainty and approval timelines can have an important influence on the economics of a project. A recent CERI study found that permitting timelines for petrochemical plants are twice as long in Alberta as in the US, and even longer in Ontario. In this industry, provinces and states have a relatively high degree of influence on permitting. In US Gulf Coast states like Texas and Louisiana, states have services available to streamline permitting processes and reduce uncertainty, making the regulatory environment more favourable to investors.

Exports

The market for petrochemicals in North America is now fairly saturated, and demand growth is being driven by Asian markets. This is a positive trend for North American producers, as increasing demand has allowed the industry to grow. However, it also means that access to these markets determines revenues. CERI analysis found that netback prices were higher in the US than in Canada because of Gulf Coast access to shipping terminals.

Other chemical manufacturing

As noted in the introduction to this section, the category we refer to as “other chemical manufacturing” is a composite of several smaller industries. These industries are cosmetics, soap, adhesives, paint, fertilizer, synthetic fibres, and other chemicals. For these industries, details of the cost competitiveness between Canada and the US are not available. In order to supplement this data, we have used information gathered from interviews with industry participants. Based on these interviews, we understand that prior to US tax reform, Canada and the US were roughly equally attractive to investment in other chemical manufacturing. This means that US tax reform could be a deciding factor in where to locate investment.

The following identifies key trends that are influencing competitiveness in the industry now and in the future.

Low growth

With few exceptions, growth in this industry is predicted to be fairly low, often less than 1% per year. Producers in Canada and the US are focused on the North American market, which is fairly mature and saturated. Therefore, volume is unlikely to drive future growth in the industry. Instead, companies will need to innovate in terms of product customization and lower costs. In 2017, the industry saw a high volume of M&A activity as a means to consolidate and drive growth. These trends are one reason for the focus on greater digitization and automation described below.

Industry 4.0

As in many manufacturing industries, future investments will be heavily influenced by a drive towards digitization and automation. A recent survey by PwC found that chemical manufacturing companies plan to invest 5% of annual revenue in digitization over the next five years, and almost one third say they are already at an advanced level of digitization. Interviews with industry members confirmed that chemical manufacturing companies operating in North America are actively piloting and developing advanced digital manufacturing facilities. In addition to the low-growth environment in the industry, labour markets are another issue driving automation. It is difficult for companies to hire reliable factory labour at low wages, and outsourcing to regions with lower labour cost represents a short-term gain. Automation provides an opportunity to “onshore” manufacturing and locate closer to customers and supply chains. It can also enable greater customization and more responsiveness to consumer preferences. In this way, companies can increase revenue while decreasing costs.

Other factors

- Government incentives. As in other manufacturing industries, many federal and state/provincial governments offer incentives for investment that creates new jobs. This can be a motivating factor in deciding where to locate investment.

- Proximity to markets. Chemical manufacturing in Canada and the US is focused on the North American markets. Proximity to customers lowers transportation costs and allows for more flexibility in meeting demand. Uncertainty around trade and tariffs in North America.

- Access to talent. Skilled labour is an important factor and will become even more crucial as automation and digitization increases. Currently manufacturing regions in both Canada and the US provide a good supply of skilled labour.

Investment decisions

The following outlines our understanding of the important factors when deciding where to locate a new chemical manufacturing plant:

- Feedstock availability and price. The price of feedstock and proximity to manufacturing facilities is the most important factor for petrochemical manufacturing. Feedstock accounts for around 70% of operating cost. In Canada this is largely driven by the price of natural gas, and in the US the price of crude oil is also a factor.

- Regulation and permitting timelines. Uncertainty, complexity, and length of permitting processes can influence the economics of a project. Canada has longer and more complex processes than the US Gulf Coast. In other chemical industries, greater harmonization between Canada and the US would support this export-intensive industry. Additionally, anecdotal evidence suggests that permitting timelines are longer in Canada.

- Access to market. Because most demand growth is coming from Asian markets, cost of transportation and time it takes to get to market are important. Currently the US Gulf Coast has an advantage over Canada because of its proximity to ports.

- Labour costs. Labour costs can also affect profitability, but not as much as feedstock. Shortages in skilled trades in Alberta, for example, can make it less attractive to investors.

- Access to skills. Skilled labour is very important to industry performance and is becoming more important as automation and digitization increase.

- Government incentives. As noted above, government incentives have influenced recent investment in both Canada and the US. Generally, incentives provided in the US are more generous.

- Taxes. Taxes could be a deciding factor in where new investment is located, especially given that Canada already has a disadvantage in terms of costs.

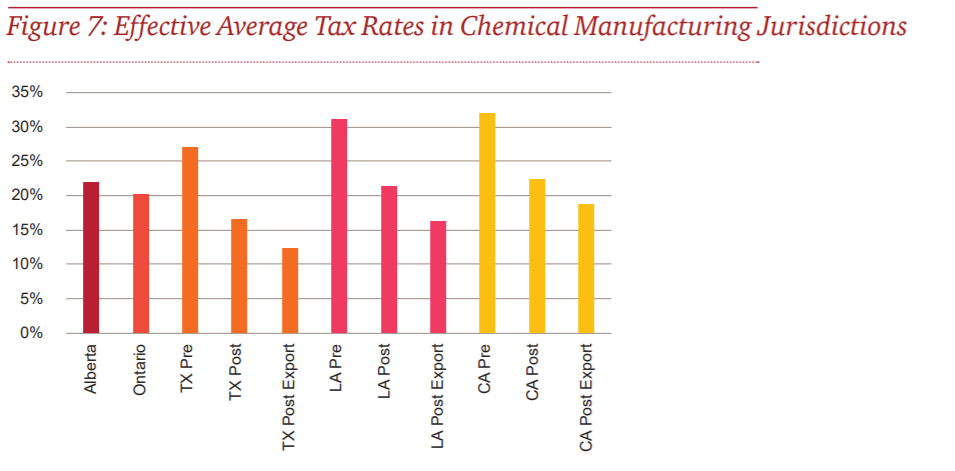

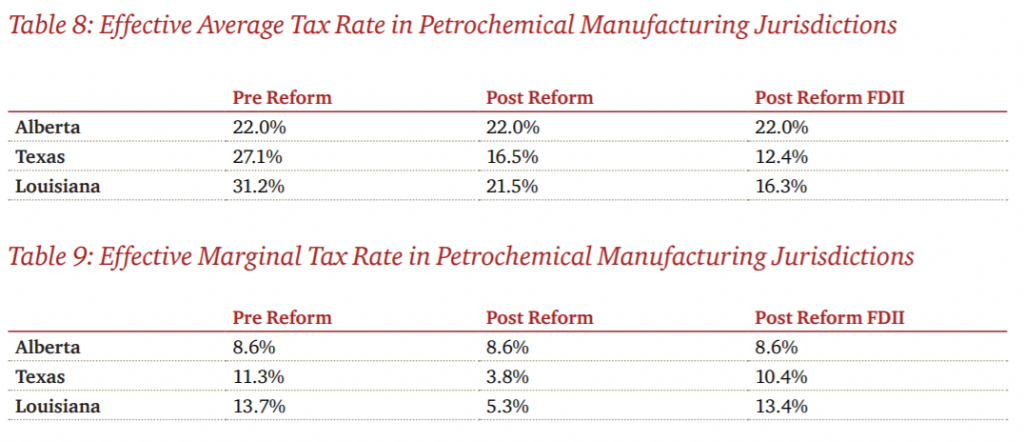

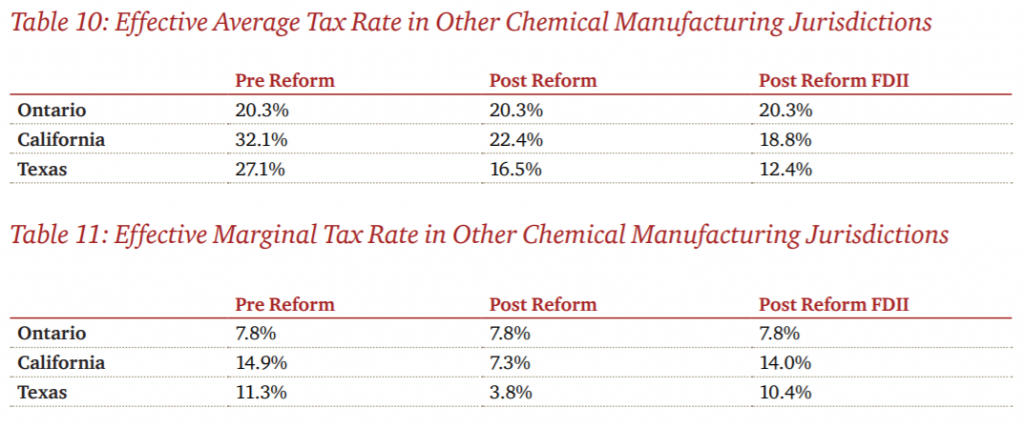

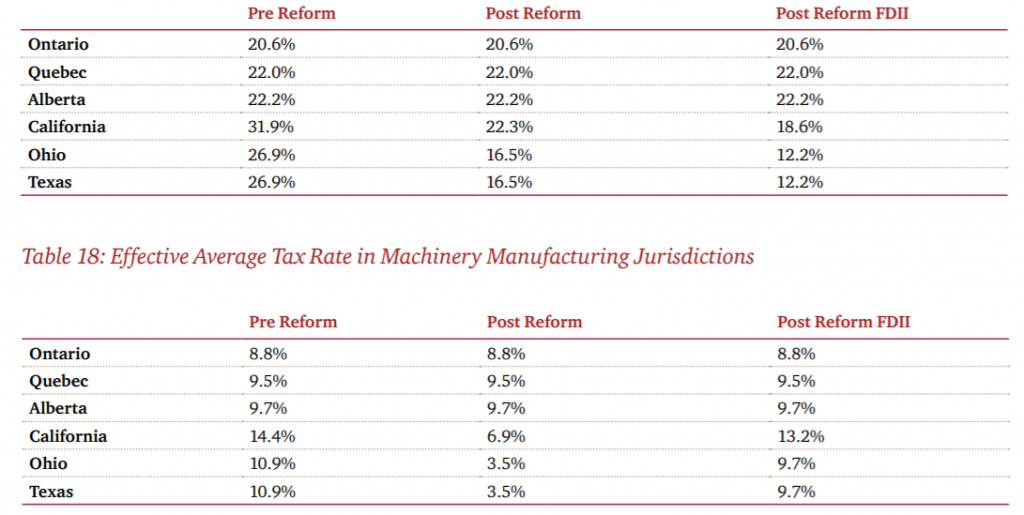

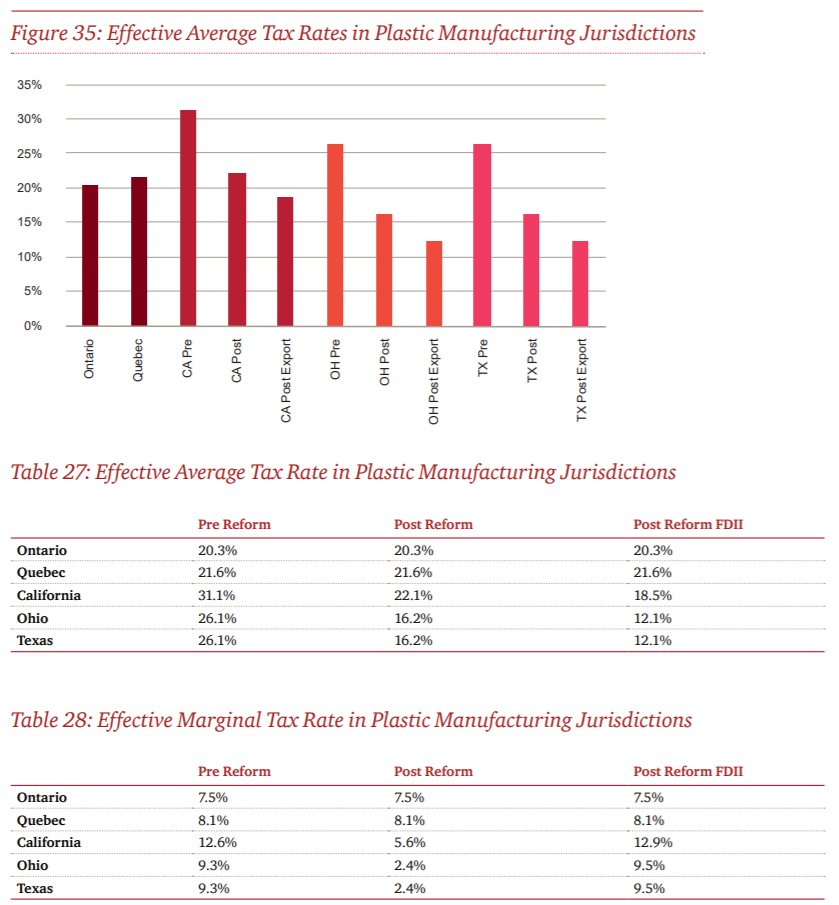

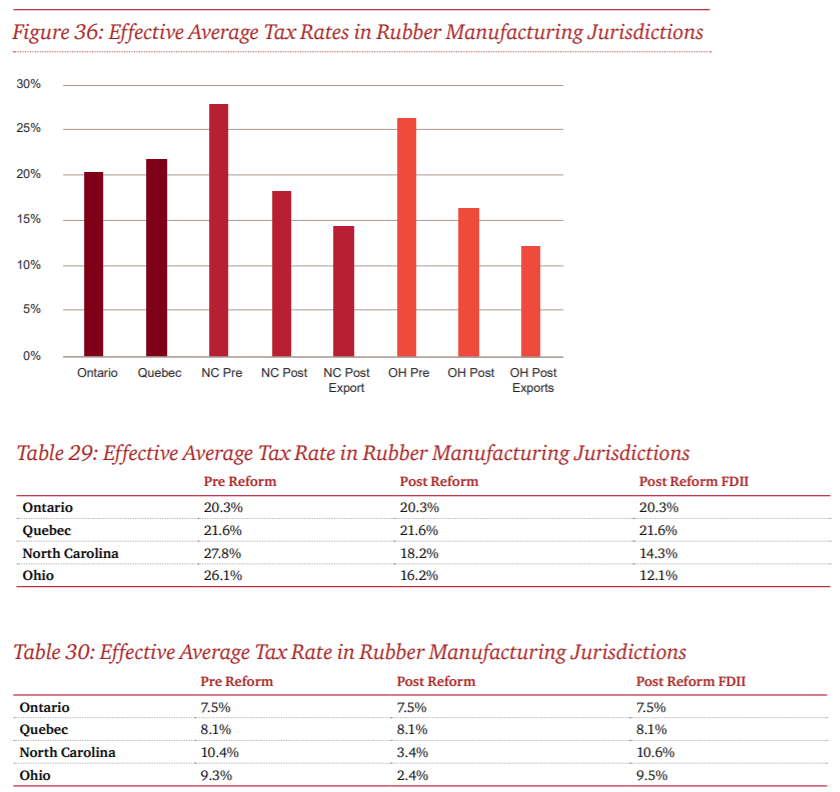

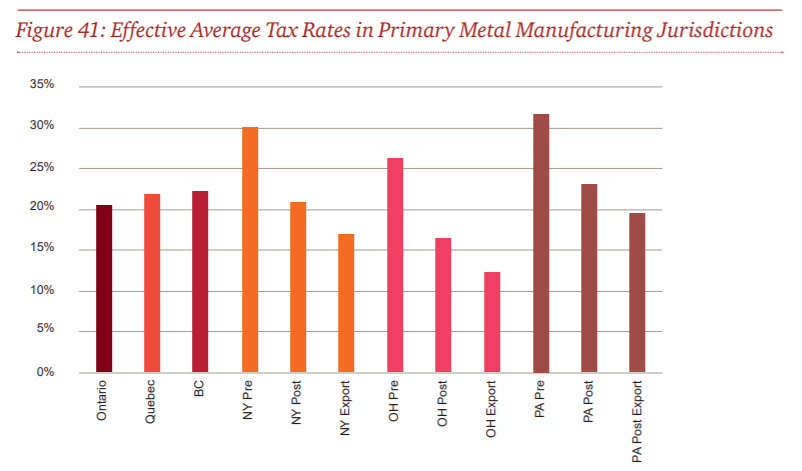

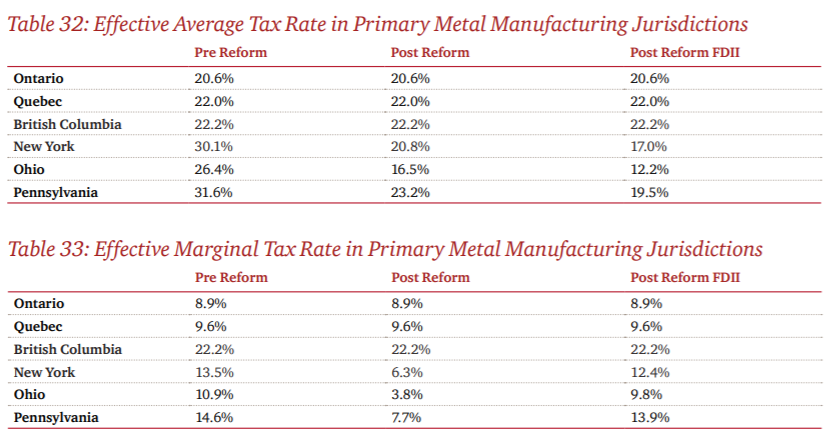

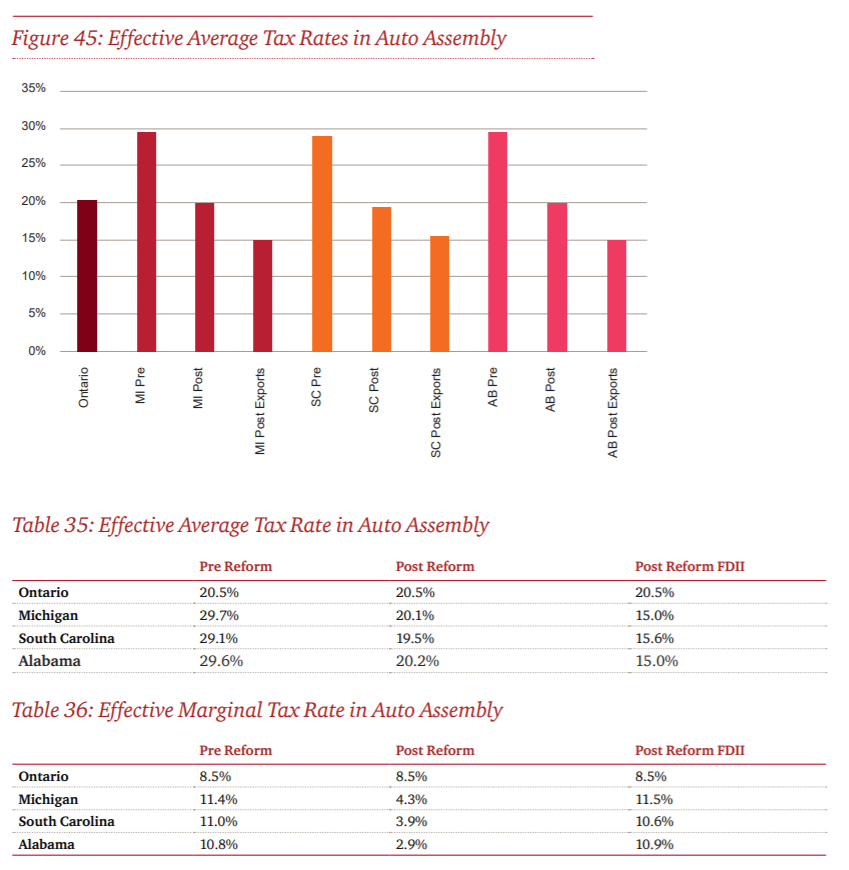

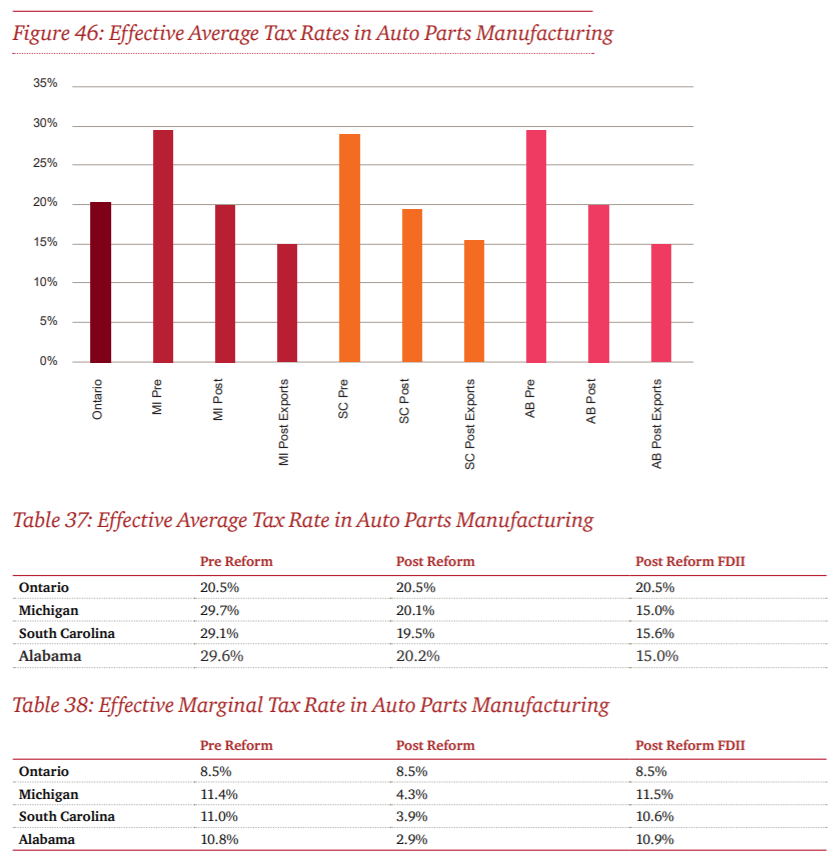

Tax impacts

The figure and tables below presents the effective average tax rates and effective marginal tax rates in chemical manufacturing jurisdictions.

The jurisdictions included here are Alberta, Ontario, Texas (TX), Louisiana (LA) and California (CA). For more details on tax rate calculations, see Appendix B: Tax analysis methodology.

Petrochemical manufacturing

The following tables present the effective average tax rates and marginal average tax rates in petrochemical manufacturing jurisdictions.

Other manufacturing

The following tables present the effective average tax rates and effective marginal tax rates in the principal jurisdictions for other chemical manufacturing.

Rate of Return

In the petrochemical industry, our analysis suggests that Canada had a higher pre-tax rate of return prior to the US tax reform. Post-reform, Canada’s advantage in post-tax return is eliminated. As noted above, the potential development of a liquefied natural gas facility on Canada’s west coast creates a risk of increasing natural gas prices, thereby making Canada less competitive, as this is the primary input into Canada’s petrochemicals.

In the other chemical manufacturing industries, jurisdictions in Canada had a lower after-tax rate of return compared to California and Texas. The US advantage has increased significantly post-US tax reform.

Likely expectations

Taking all of the above into consideration, we are of the view that the US tax reform, all else being equal, poses a substantial risk to the long-term viability of all of Canada’s petrochemical industry and other chemical industry. In particular, we have developed the following likely expectations regarding the effects of the US tax reform on the chemical manufacturing industry in Canada:

- Methane and ethane-based petrochemical manufacturing is at a serious risk in Canada.

- There is potential planned investment of $20 billion CAD in Canada in the next few years, suggesting that there could be a major short-term impact if these projects are affected.

- Cost of construction of petrochemical facilities is higher in Canada.

- The building of an LNG facility could threaten Canada’s petrochemical competitiveness by raising the cost of natural gas, the key input in production.

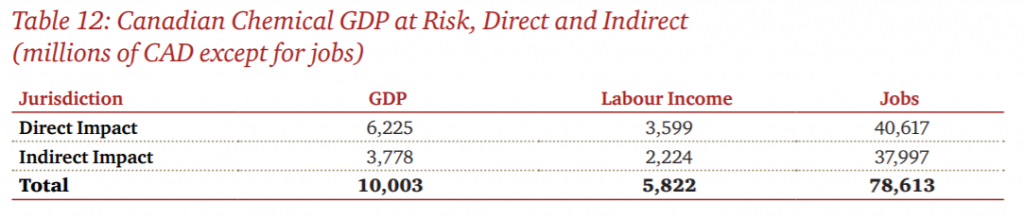

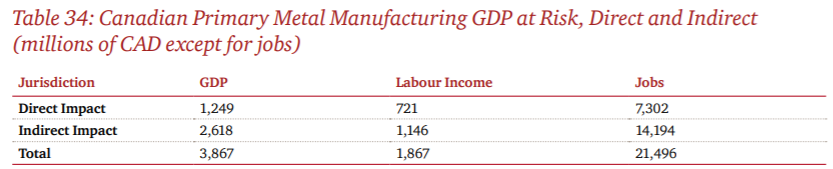

The table below shows the portion of this sector that is “at risk” based on our assessment. These figures include the direct economic footprint of petrochemical and other chemical manufacturing industries in Canada, and the associated indirect, or upstream economic impact. We assess that a large portion of these industries will be at risk in the long term. We represent this view numerically by suggesting that 75% of the total economic footprint of these industries is at risk.

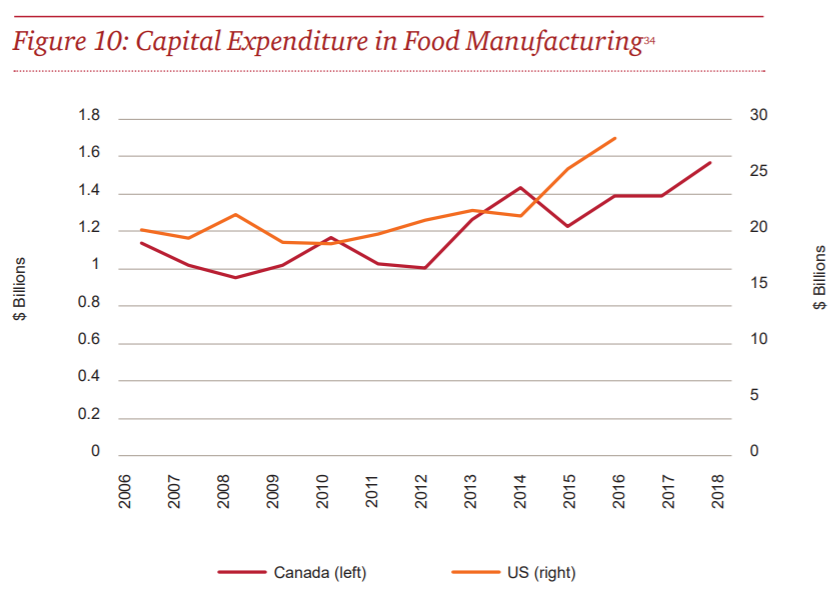

Food manufacturing

The food manufacturing sector produces food for human or animal consumption. The susceptibility of each type of food manufacturing to US tax reform will depend on the nature of their products. Typically, products with high value-to-weight and long shelf life are profitable to export, whereas other types of food are produced only for domestic consumption. For this reason, we have narrowed our analysis to the following industries:

- Flour milling

- Margarine and cooking oil processing

- Cereal production

- Chocolates, candy and ice-cream production

- Frozen food production

- Cookie, cracker, pasta, snack food production.

Together, the above categories account for approximately 20% of revenue.

We have excluded the following industries from our analysis:

- Production of dairy products and poultry processing: these are low value-to-weight products, and trade is closely regulated under supply management.

- Animal food and other (non-poultry) meat processing: these products are low value-to-weight and exports to the US are low.

- Seafood production: it is resource-bound in Atlantic Canada.

- Bread production: due to low shelf life, it is difficult to transport.

- Canned fruit and vegetable production: typically, the production needs to be close to farms.

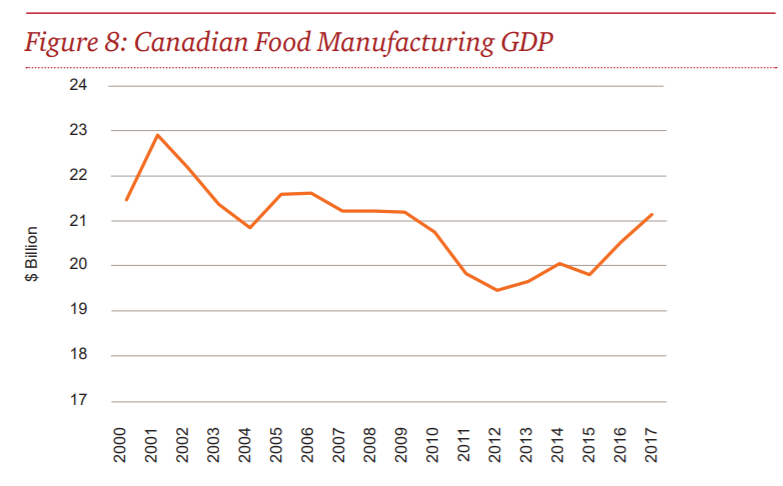

Food manufacturing in Canada

GDP in Canada’s food manufacturing industry has been increasing since a low in 2012. Ontario and Quebec are the centres of food manufacturing, accounting for 44% and 21%, respectively, of miscellaneous food manufacturing. They are followed by Saskatchewan, Alberta and British Columbia.

Food manufacturing in the U.S.

Food manufacturing represents a similar share of the overall economy in the US and Canada. In the US, foodmanufacturing GDP has been increasing steadily since 2011, showing a trend similar to that in Canada over this time. Food manufacturing facilities are concentrated in California, Texas, Illinois and Ohio.

Investment trends

Since around 2010, capital expenditure in food manufacturing has been increasing both in the US and Canada. The data below includes the entire food manufacturing sector, so may not be representative of the industries we are focusing on in our analysis. Our research suggests that, US food manufacturing capex has continued to grow since 2016, although more slowly than in the past. The expected increase in planned investment from 2017 to 2018 is 2%.

Key sector trends

The following key industry trends are important for the long-term competitiveness in Canada and the US for food manufacturing facilities in the industries we have identified as vulnerable:

- There are two conflicting trends in food prices: i) downward pressure due to competition and ii) upward pressure as high-value added products and quality become increasingly important. Thus, the two key business strategy considerations are: i) product innovation and ii) cost containment.

- A key challenge is legal requirements regarding food safety, labelling and traceability, and other trade regulations.

- According to a survey, around 20% of industry participants believe that food production can be largely automated in 30 years. Therefore, this industry is likely to be affected by automation, but less so compared to other industries examined in this report.

Investment decisions

The following outlines our understanding of the important factors when deciding where to locate a new food manufacturing plant:

- Proximity to raw materials. This is the primary factor when considering a location for food processing facilities is proximity to market and raw materials.

- Access to market. Currently trade barriers are low within North America, meaning that export opportunities within North America are strong in both Canada and the US.

- Transportation cost. This sector also tends to be located in the most populous jurisdictions in both Canada and the US in order to minimize transportation costs.

- Labour cost. As in other manufacturing industries, labour cost is an important factor and has led to the consideration of automation opportunities.

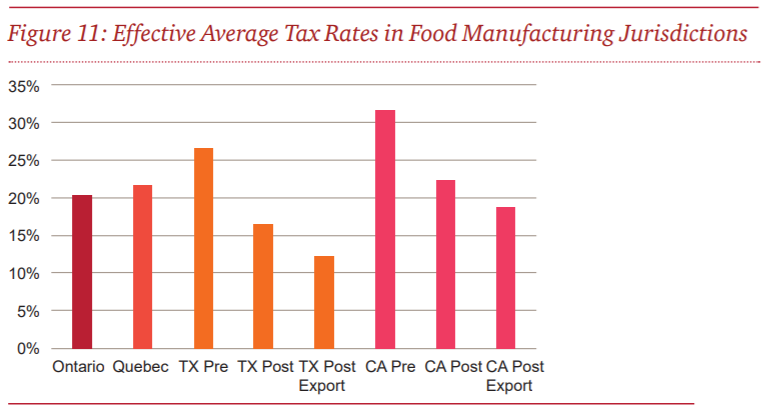

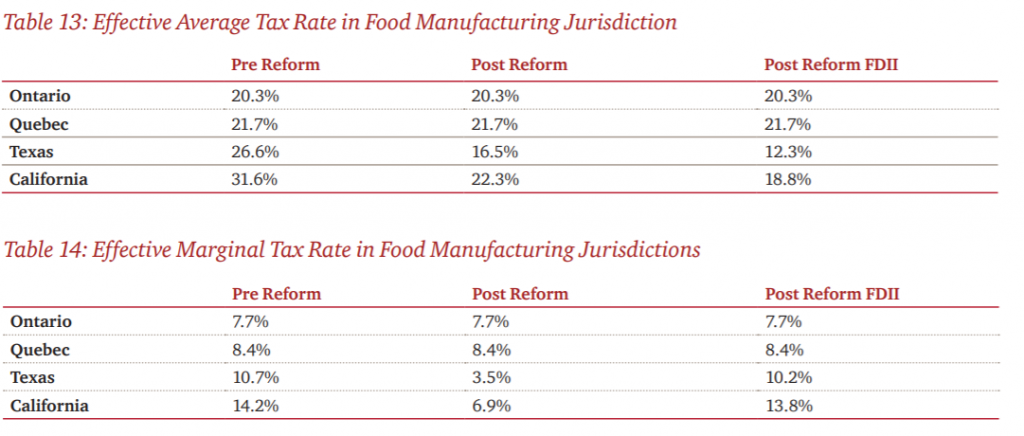

Tax impacts

The following chart and tables present the effective average tax rates and effective marginal tax rates in food manufacturing jurisdictions.

The jurisdictions included here are Ontario, Quebec, Texas (TX), and California (CA). For more details on tax rate calculations, see Appendix B: Tax analysis methodology.

The following tables present the effective average tax rates and effective marginal tax rates in the principal jurisdictions for food manufacturing.

Rate of return

Based on our analysis, profits in food manufacturing industries we have studied are on average substantially higher in Canada than in the US; although the reasons for this are not entirely clear, this trend was stable over time. This is the case for all industries within food processing except for chocolates, candy and ice cream production and cookie, cracker and pasta manufacturing, where profits are similar between Canada and the US.

Likely expectations

Our view is that US tax reform will have a small negative impact on affected food manufacturing in the short term and a moderate negative impact in the long term. The reasons for this view are the following:

- Regulations in Canada are more stringent than in the US, making it less attractive to investors.

- Barriers to trade are very low, so US facilities can serve the North American market.

- High capital intensity means that immediate capital expensing is very beneficial.

- After tax return in Canada will continue for the most part be higher than in the US.

The table below shows the portion of this sector that is “at risk” based on our assessment. These figures include the direct economic impact of the food manufacturing sector in Canada and the associated indirect, or upstream economic impact. We assess that 80% of this sector is unlikely to be impacted by US tax reform because, as described above, these industries primarily serve the domestic market and it would not be practical to move facilities to the US. The remaining 20% is likely to experience a small negative impact. We represent this view numerically by suggesting that 2% (10%*20%) of the total food manufacturing economic footprint is at risk in the long term.

High-tech Industries

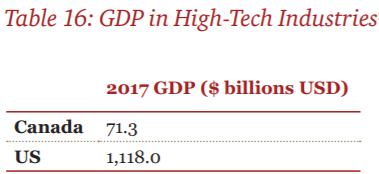

The high-tech industry is not identifiable using the NAICS codes that we have used for other industries. The OECD has estimated the GDP of the high-tech industry by aggregating ICT manufacturing, telecommunications, software publishing, and IT and other information services. The table below shows the estimated high-tech GDP in Canada and the US based on this definition.

The software industry is increasingly important in today’s digital economy and includes subsectors such as fintech, healthtech, internet of things, cloud computing, mobile, artificial intelligence, cybersecurity, and other areas of emerging technology. Telecommunications is also considered part of the high-tech sector because it is important in enabling digital technology. However, because of the increasing importance of digital technology, the high-tech industry permeates the whole economy including traditional industries such as financial services, retail, manufacturing, automotive, forestry, mining, and more.

This sector is also one of the fastest growing, and one of the most active investment targets worldwide. It is expected to be a key component of future productivity increases and growth as developed countries move towards serviceoriented high value-added economies.

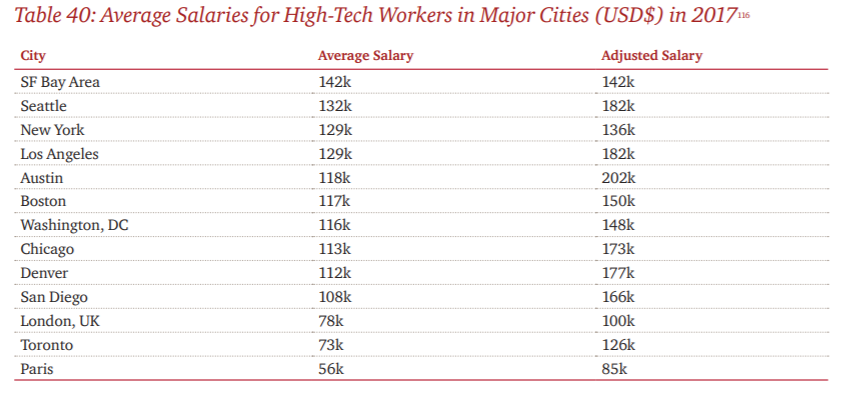

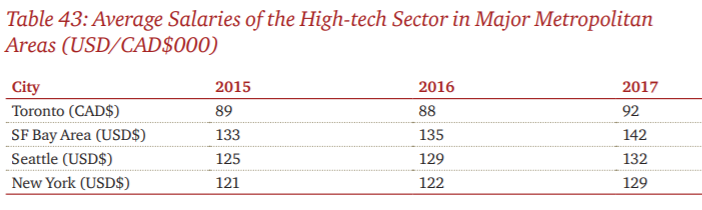

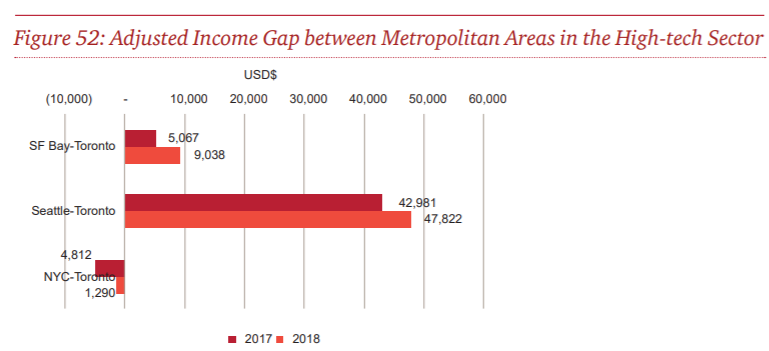

One of the most important determinants of success for both small and established companies is access to talent. Globally there is a shortage of workers with the skills needed for this sector, and competition between companies is fierce. Top tech-job markets in North America include Toronto, New York, Seattle, Washington, and the Bay Area. Average salaries, cost of living, personal income tax rates, immigration policy, and career opportunities are all important determinants of access to talent for a given company.

Along with talent, a key element of success is the funding needed for rapid growth. Venture capital (“VC”) is the most important source of funding in this sector. Although US VC firms invest in Canada, firms located in the US find it easier to attract VC funding. Currently, Toronto, Montreal, Vancouver and Waterloo attract most of the VC funding in Canada. Each market has seen an increase between 106% and 672% in in total venture capital funding over the last eight quarters.

Small high-tech companies

Most companies in the high-tech sector are small: 86% of firms in this industry have fewer than 10 employees. Many startups do not have any revenue or profits, so tax is not a consideration in where to initially locate. The lower cost of rent and lower salaries may make it more attractive to initially locate in Canada. However, lower salaries along with relatively high personal income tax rate also make it difficult to attract and retain talent.

For small firms, funding from VC and private equity (“PE”) funds are important for growth. Small-scale companies are heavily dependent on US-based VC funds in particular. These firms would be hurt if US-based VC funds decided to reallocate investments toward the US and away from Canada. We spoke to several VC firms, and most were not planning to reallocate investment towards the US. One firm that was interviewed cited US tax reform as a minor factor. Notwithstanding, we note that there was a 7% decrease in total funding to Canadian venture-backed companies between the first and second quarters of 2018, but do not have evidence to suggest that this was linked to the US tax reform.

Large high-tech companies

Some Canadian tech companies have grown to be competitive on a global stage. However, it is generally the case that when a Canadian start-up grows to a revenue level that proves the viability of its concept, its operations substantially move to the US. This is due to greater access to VC funding and often the benefits that come with being part of a larger industry cluster such as the Bay Area. Taxes are also more likely to be a concern for companies with revenue levels that produce significant profits, but, as with small companies, access to capital and talent remain the most important determinants of success and hence location selection.

Many large US-based tech companies will set up a “backup” office in Canada, because of difficulty with the immigration status of workers hired from overseas. This suggests two things: that Canada’s immigration system is more conducive to hiring high-skills workers from abroad, and that this is not a barrier to US-based companies attracting these workers and eventually bringing them to the US.

Likely expectations

We are of the view that US tax reform will have a relatively small negative impact on the high-tech sector in the short and long term. The main reasons for this are the following:

- The most important factors for tech companies are access to talent and funding.

- Start-up companies are generally unprofitable and thus tax is not a consideration.

- Larger firms already tend to move to the US as they grow due to access to funding and talent.

- The US remains an attractive destination for tech companies that reach a certain size due to greater access to talent and funding.

- Some VC firms are re-allocating investments to the US for reasons that may include US tax reform.

- We note that decreases in US personal income tax rates have made it marginally easier for US companies to attract talent. We discuss this aspect in more detail later in the section on Impact on brain drain.

Due to lack of data availability for this industry, we have not quantified the economic impacts of negative effects on this sector caused by US tax reform.

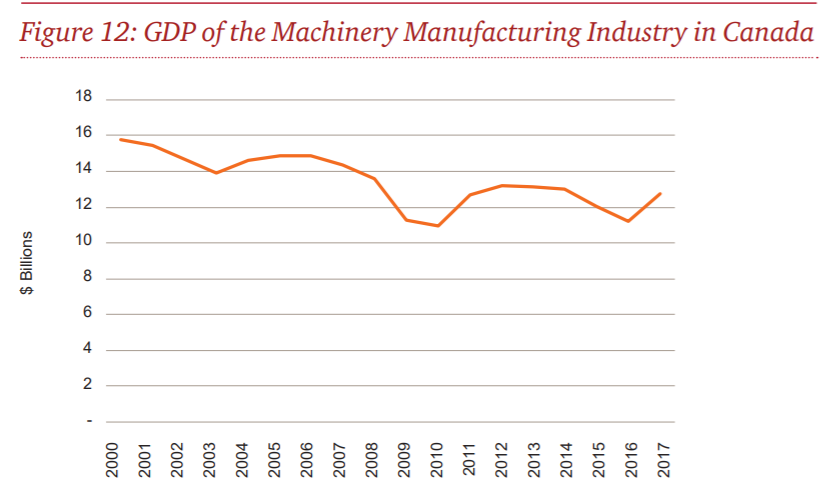

Machinery Manufacturing

The machinery manufacturing sector includes a wide range of machinery that serves various other industries. Industries we have studied are mining, oil and gas machinery; pumps and compressors; tractors and agricultural machinery; construction machinery; plastics and rubber machinery; semiconductor machinery; heating and air conditioning equipment; metalworking machinery; printing, paper, food, textile and other machinery; engine and turbines; and wind turbines.

Machinery manufacturing in Canada

Machinery manufacturing in Canada mainly takes place in Ontario and Quebec, although some manufacturers are located closer to their downstream customers, such as oil and gas machinery in Alberta and agricultural machinery in Saskatchewan. The Canadian economy is specialized in machinery-intensive industries—agriculture, minerals, oil and gas, utilities, construction and manufacturing (“AMUCM”) account for approximately 30% of GDP and companies in these activities spend almost $41 billion on machinery and equipment. Canada is a net importer of machinery and equipment, and both imports and exports have been increasing since 2010.

GDP in this sector declined from 2014 to 2016, increasing again in 2017. These movements are related to trends in the oil and gas industry, which is a major downstream consumer of machinery in Canada. Of all machinery manufacturing industries, oil and gas-related machinery posted the strongest growth in 2017.

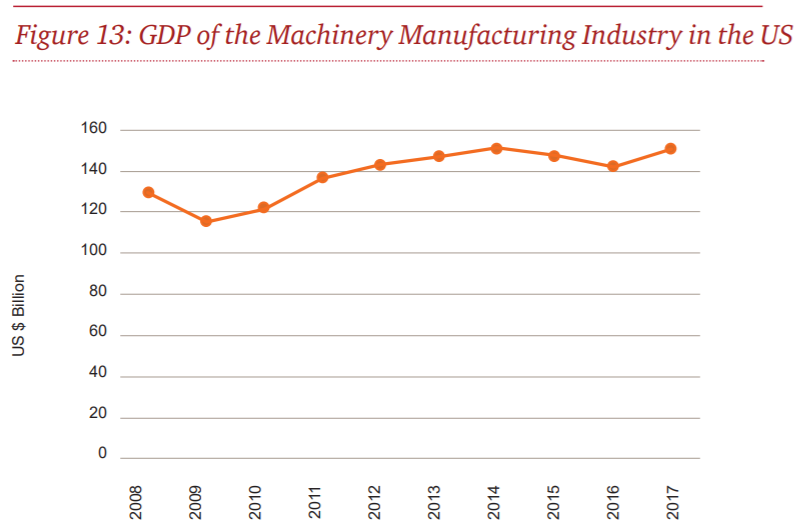

Machinery manufacturing in the U.S.

Machinery manufacturing is one of the largest and most competitive sectors of the U.S. manufacturing economy. The competition is highly globalized, and international trade is large part of revenue of the machinery manufacturing in the US.

There is some machinery production in most states, but it is concentrated in the industrial Midwest, California and Texas. As in Canada, GDP increased in 2017, reversing the downward trend of the past few years.

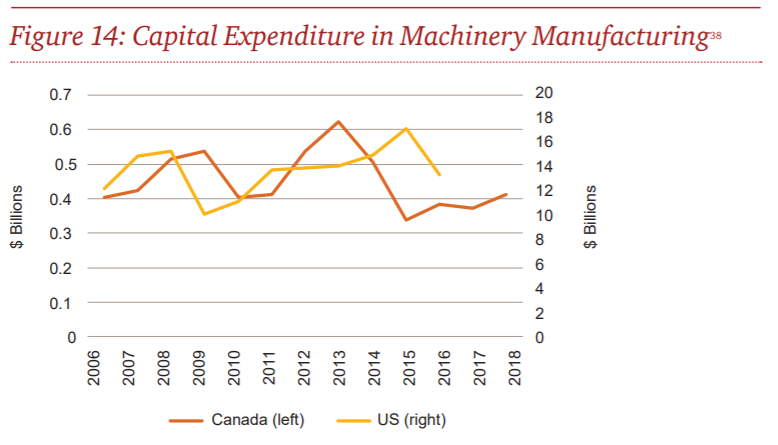

Investment trends

Capital expenditure in Canada has been declining since 2013. In the US, capital expenditure has also been decreasing even though GDP and exports have been increasing. This decline is likely related to the drop in oil prices and subsequent decrease in demand for oil and gas machinery.

Our research suggests that US capital expenditure has been increased modestly or remained flat since 2016, depending on the industry.

Key sector trends

The following section reviews key trends in the industry that are important to understanding the context of the impact of tax reform.

- The growth of demand in emerging markets. The clearest trend from the past decade is the growth of emerging economies both as consumers of manufactured goods and competitors or collaborators in producing them. This means that access to the international market is a crucial factor of firms’ competitiveness in this industry. Transportation infrastructure and trade policy can both have a major impact.

- Industry 4.0. Automation is increasing in the design, production, and marketing of manufactured goods. Industry 4.0 has the potential to dramatically reduce costs and improve productivity, but will require substantial additional capital investments. Firms expect to more than double their level of digitization by 2020 from 33% now to 72% by 2020.

- Downstream demand. Machinery manufacturing is highly fragmented, as demand for each type of machinery is determined primarily by its downstream use, which varies by type of machinery. For example, demand for oil and gas and mining machinery is closely linked to commodity cycles in those industries. Demand for wind turbine machinery is determined by overall trends in energy markets, and by government programs and incentives.

Investment decisions

From discussions with industry members, we understand that the following factors are important determinants of investment decisions.

- Access to market. Foreign markets are currently a major source of growth for the industry in Canada and the US. Therefore, access to the international market, such as low trade barriers and well-developed infrastructure, is a key determinant of firms’ investment decisions.

- Trade barriers. Currently Canada has an advantage due to lower trade barriers; Canada has a duty-free manufacturing tariff regime and is the first country in the G20 to offer a tariff-free zone for industrial manufacturers. In 2015, Canada implemented a major new initiative that reduced tariffs on all manufacturing inputs to zero, which will benefit machinery manufacturing by lowering the cost of imported inputs. On the other hand, the US recently raised tariffs on machinery components from China, a major supplier and consumer of the machinery manufacturing industry.

- Transportation. Canada and the US both have well-developed transportation infrastructure. According to the International Logistics Performance Index (“LPI”), Canada is ranked 17th best for logistics infrastructure, while the US is ranked 10th. However, in some cases international suppliers have been chosen over Ontario manufacturers in supplying machinery to Alberta due to lack of oversized load corridors.

- Cost factors. Access to labour and primary metal inputs, as well as the exchange rate, all contribute to overall competitiveness.

- Taxes. Given the trade-intensive nature of the industry and the similar cost structure in Canada and the US, taxes could be a deciding factor.

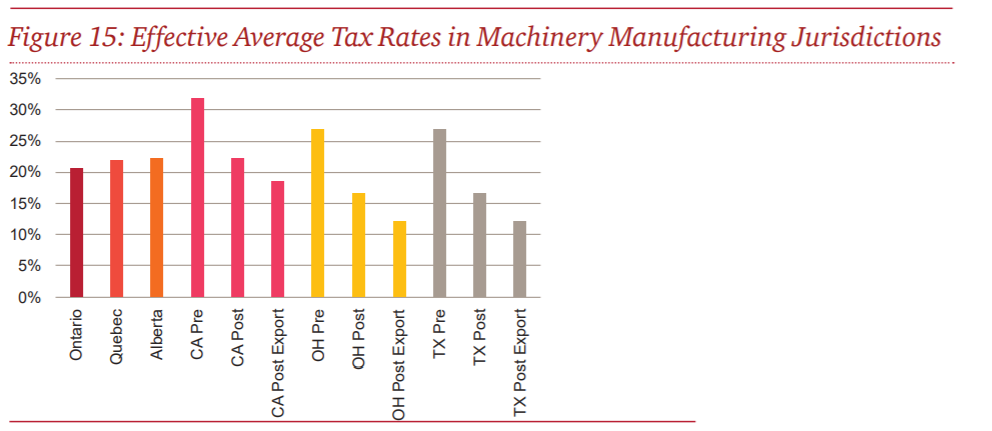

Tax impacts

The following figure and tables present the effective average tax rates and effective marginal tax rates in machinery manufacturing jurisdictions.

The jurisdictions included here are Ontario, Quebec, Alberta, California (CA), Ohio, (OH), and Texas (TX). For more details on tax rate calculations, see Appendix B: Tax analysis methodology.

The following tables present the effective average tax rates and effective marginal tax rates in the main machinery manufacturing jurisdictions.

Rate of return

Overall, Canada and the US are currently fairly competitive. Our analysis suggests that with some exceptions, machinery manufacturing industries in Canada and the US have similar pre-tax rates of return. Prior to the US tax reform, after-tax return was higher in Canada. Post-US tax reform, with the exception of two industries, the US has a significantly higher after-tax rate of return. The two exceptions are tractor and agricultural equipment and pump and compressor manufacturing, which still enjoy higher rates of return postUS tax reform. These two industries account for 21% of revenue in the machinery manufacturing sector and 21% of exports.

Likely expectations

Taking all of the above into consideration, we are of the view that the US tax reform, all else being equal, will have a small negative impact on about 80% of the machinery manufacturing sector in the short term and a large negative impact in the long term. The reasons for this are the following:

- This industry is capital-intensive and will require additional capital investment as Industry 4.0 progresses.

- The rising trade barriers between the US and other countries may dampen the inflow of investment back to the US in the short term.

- The industry is export-intensive in both countries, and the North American market is highly integrated. Therefore, manufacturers located in either country could serve North American and international downstream industries such as agriculture, minerals, and oil and gas.

In summary, a combination of demand from downstream industries and relatively high market access could keep investment in Canada in the short term. In the long term, the US tax reform provides incentives for machinery manufacturers to relocate their investment to the US, and the overall impact will be significant if US barriers to trade are lowered.

The table below shows the portion of this sector that is “at risk” based on our assessment. These figures include the direct economic impact of machinery manufacturing sector in Canada, and the associated indirect, or upstream economic impact. The footprint below excludes the two industries that we have identified as not being at risk (tractor and agricultural equipment and pump and compressor manufacturing). Based on our analysis, a large portion of these industries will be at risk in the long term. We represent this view numerically by suggesting that 75% of the total machinery manufacturing economic footprint is at risk.

Green technology

The green technology sector includes all activities aimed at reducing carbon emissions and environmental impact such as renewable energy generation, storage and transmission, and efficiency-enhancing technologies. According to Statistics Canada, sales of this sector were $3.8 billion CAD in 2015. Green technology is a growing part of many sectors discussed in this report, such as environmentally friendly chemical manufacturing and electric vehicle

manufacturing.

While there is strong potential for growth in the green technology sector, in Canada this sector is still in early stages. According to a report by Analytica Advisors, R&D activity in the sector is strong, but businesses are having difficulty scaling. The authors also revised their expectations of the sector’s growth downward from previous years’ reports. The Canadian and provincial governments have offered support and incentives for green technologies. For example, in the 2017 budget, the federal government announced $2.3 billion in support for clean technology, which is available under a range of programs. However, we note that recently the Ontario government has withdrawn most of its support for this industry.

There is limited information on the competitive of Canada’s green technology sector relative to the US, as green technology is a part of many different sectors. One specifically “green” industry we assess is wind turbine manufacturing, which is a part of the machinery manufacturing sector. Our analysis suggests that a large part of this industry is at risk due to US tax reform. Generally speaking, we expect green technology, particularly those related to manufacturing, to be negatively impacted by the US tax reform.

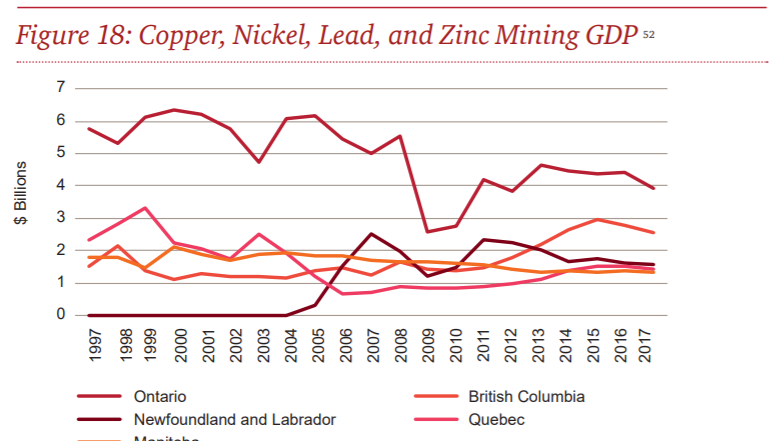

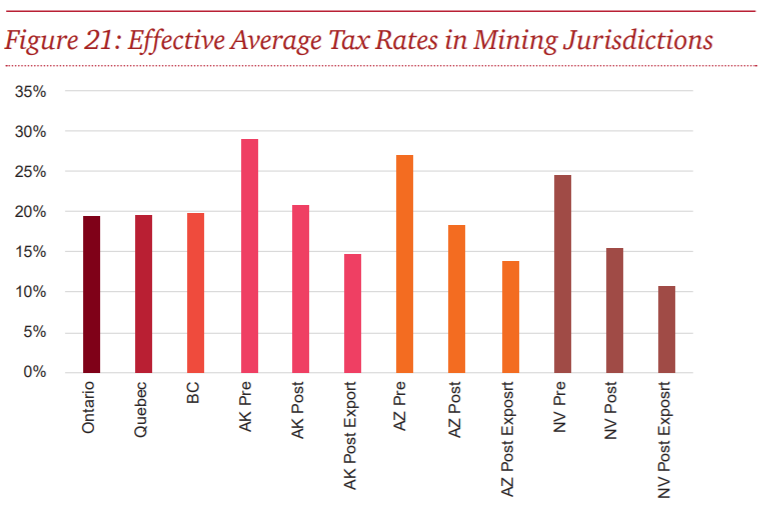

Mining

The mining sector is engaged in extracting metals and minerals from the earth, and exploration to assess sites of future investment (junior mining). It includes coal, but not oil sands mining. Canada and the US are both top mining jurisdictions globally. In 2017, Canada attracted the highest share of global exploration investment at 14%, while the US was in third place with 7%. The mining industry is highly globalized, and typically large companies are engaged in exploration activities around the world. Other major mining regions include Australia, South America and China.

Both the US and Canada produce dozens of metals and minerals. However for the purposes of this report, we have narrowed our analysis to the metals and minerals that are significant to the US and Canada and for which the US and Canada are competing for capital investment. To do so, we applied the following criteria:

- Minerals that make a substantial contribution to GDP in both countries.

- Minerals that do not rely heavily on close proximity to markets.

- Minerals for which there is recent active exploration and development activity in both countries.

Based on these criteria, our analysis focused on two minerals: gold and copper. While stone, sand and gravel are important industries in both countries, very low levels are exported or imported due to high transportation cost.

As noted above, mining is a globally competitive industry. Mining companies looking to develop new resources have several potential projects at any one time, and assess the economics of each before deciding where to allocate capital.

Compared to other industries assessed in this report, two main factors differentiate the type of investments made in resource industries: the length of investment decisions, and the resource cycle. A new mine may produce for 20 or 30 years and will be an economic consideration for even longer due to reclamation activities. The mining industry is also highly influenced by global commodity prices, which tend to be cyclical. The industry recently recovered from a commodity price bust and is expected to continue growing for several years.

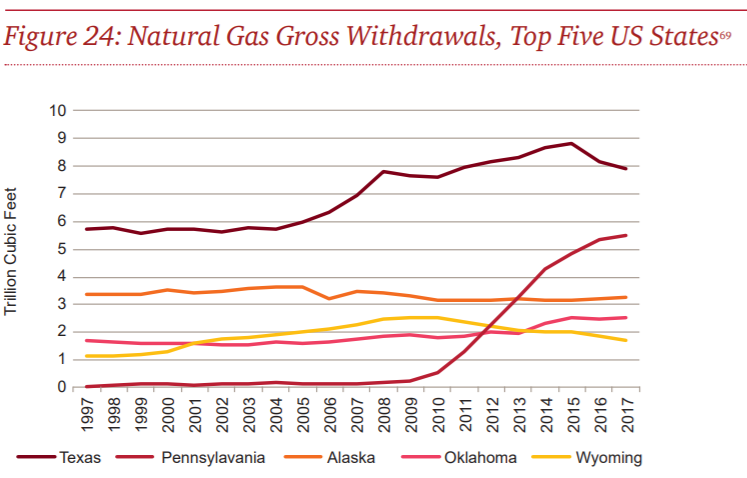

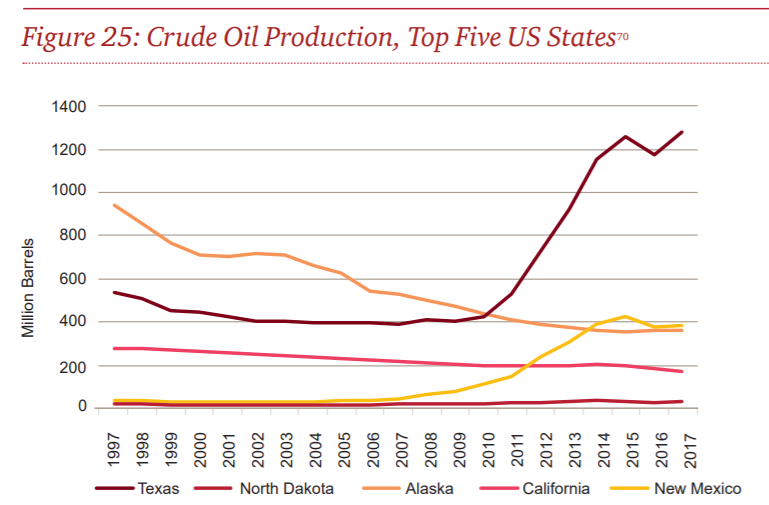

Mining in Canada